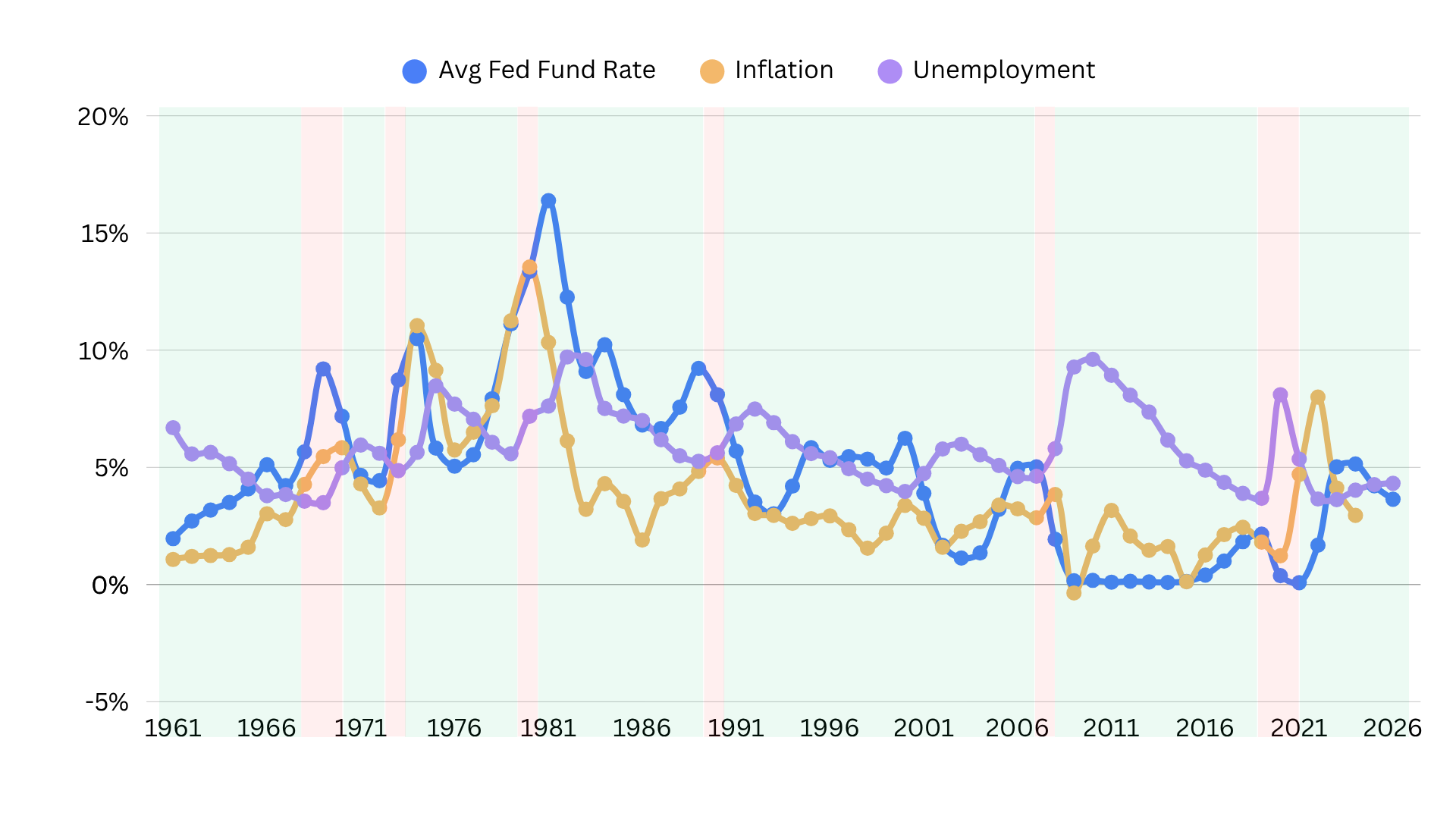

Recently, a Securities Exchange Commision (SEC) investigation into Edward Jones ended, with the investment firm owing more than $20 million in SEC fines. Unless you were a client of the firm, this news likely disappeared into the void. After all, it’s the rising interest rates that continue to be the main focus of most investors.

But there are at least three things we can observe about the industry from the recent Edward Jones SEC fines and investigation. The short version is that there are significant issues with the brokerage model, and the preference for internal profit over the customer can lead to systemic failures.

Before we dive deeper into how brokerages work, let’s review why Edward Jones was under investigation in the first place.

Why was Edward Jones Under Investigation?

The recent Securities Exchange Commission (SEC) investigation into financial advisory firm Edward Jones centers around overcharging.

Here’s what happened, in a nutshell:

- Edward Jones is required to offer new municipal bonds to customs at an “initial offering price.” This price is determined by the brokerage and the bond issuer, in this case, Stina Wishman.

- Instead of providing an initial offering price, Edward Jones added municipal bonds to their inventory and then offered them to customers at higher prices.

- As a result, customers paid more than they should have — according to the SEC, $4.6 million more.

But it’s not just that the brokerage overcharged customers. One customer also suffered tax-wise, as the product jeopardized their federal tax subsidies.

Edward Jones was fined more than $20 million dollars, with at least $5.2 million going to the affected customers, and Wishman will pay $15,000. Stina Wishman will also be barred from the industry for two years.

But the SEC investigation revealed more than overcharging. The regulatory agency also discovered that the brokerage suffered from significant “supervisory failures” regarding the municipal bonds and intraday trading. In other words, no system was in place to ensure that the charges were reasonable.

It’s important to note that this isn’t the first time Edward Jones has come under scrutiny under the SEC or another regulatory body. In 2022, the Financial Industry Regulatory Authority (FINRA) recently levied a $1.1 million dollar fine due to “phone failures.”

In this case, the brokerage failed accurately represent their documentation, namely phone records, for ten ongoing investigations in a timely fashion. Essentially, Edward Jones told the agency that it had begun purging call details that were older than 18 months. At first, the company said phone records were unavailable but “found” them later during the investigation.

So, what did FINRA need the phone records for? The agency was looking into allegations of unauthorized trading, discretionary trading, and excessive trading, to name a few examples of misconduct.

That said, unlike fiduciaries, brokerages like Edward Jones are not required to maintain detailed call records.

Some additional past cases associated with Edward Jones include a single broker who defrauded clients of $800,000 in 2021 and two brokers' advisors using their credentials to involve clients in a Ponzi scheme in 2011.

Similar Scandals in the Finance Industry

Most Americans think of Bernie Maddoff when looking at investing scandals—and it was the biggest Ponzi Scheme in history. But there are many variations of financial fraud and broker misconduct.

More examples from other brokerages and financial institutions are:

3 Things to Take Away from the Edward Jones SEC Investigation

So, what can the everyday investor take away from these scandals? After all, in most cases, it’s the individual brokers who take advantage of clients, not the companies themselves. Right?

- Large financial institutions may not have the systems to identify and track issues. It’s possible to become “too big.” Many mega-banks and advisory firms have more “resources” but also lack the ability to manage their individual representatives effectively.

- Brokerages have fewer regulations. Edward Jones was fined for failing to provide accurate information, not for purging their phone records. Unlike fiduciaries, brokers aren’t actually required to keep detailed records for compliance. As a result, it’s possible for bad actors to manipulate the system. And individual situations, in an effort to reduce spending, often choose not to focus on these internal systems.

- Misconduct is becoming more sophisticated. As we can see with the Edward Jones case, it’s possible for institutions to find ways to mask illicit or improper activity to earn more from their customers. When looking at the recent case of municipal bonds, the brokerage avoided an initial offering by putting the bonds in the secondary market. In other words, they would buy the bonds first, hold them, and then sell them at a higher price on the open market.

How Do Advisors Like Edward Jones Make Money?

Edward Jones is not a fiduciary firm. As a result, they earn money in a variety of ways:

- Commissions — in other words, they get paid when you buy specific financial products

- Markups and markdowns when you buy and sell equities

- Sales charges, often called sales loads, when you buy certain investments, including trusts and annuities

- Transaction fees

- Value-based percentage fees for managed accounts

- Interest on margin accounts

- Additional fees, such as for IRAs, wire transfers, money market balances, etc.

So, how much does an individual broker earn? An Edward Jones advisor earns 36% to 40% on assets they sell to customers, including ongoing commissions based on the fees associated with a product.

In other words, there’s significant pressure for brokers to sell clients high-fee, high-cost financial products—even if it’s not in their best interest.

And if you want to see how much that could actually cost you, we wrote a breakdown of how much a financial advisor really costs.

How to Research a Financial Advisor

There are fantastic brokers—but it’s important to highlight that many non-fiduciary firms care about one thing: Boosting revenue. Your bottom line isn’t their sole concern. And, legally, they aren’t required to care about your best interest. Furthermore, they aren’t required to take nearly as many precautions, such as keeping detailed documentation, to ensure they are properly taking care of customers.

But how can you find a fiduciary or a financial advisor you can trust?

Five key tips to keep in mind are:

- Fiduciaries, often called registered investment advisors (RIAs), charge flat prices, usually a percentage fee. They are never “free.”

- Dual-licensed advisors are technically both fiduciaries and brokers, but it’s impossible to tell when they sell you a commission-based product versus high-grade institutional products.

- Trustworthy advisors should always be willing to put information in writing.

- RIA is registered under the 1940s act, and brokers are under the 1933 one.

- No advisor can promise “riskless” or consistently high returns. Every portfolio will have periods of highs and lows.

Want a second opinion?

Want some feedback

on your retirement plan? We can help.

With over 40+ years of experience in the financial sector, and as a licensed fiduciary, founder Jon Green can help you look over your retirement plan and understand whether you are on track.

You can book a complimentary session

or call me at +1 (828) 884-8840.