People often refer to it in a negative context, especially in news media commentary and discourse, but what does it mean? How complex is it, really? And how can investors preserve the value of their assets?

The fact is, while inflation causes a host of problems for investments, there are silver linings depending on the particular cause for it. Furthermore, there are much worse things, such as hyperinflation and deflation, which we'll tackle later.

Before we get into the nitty-gritty, let's cover what inflation is in the first place.

The basics of inflation

Inflation is the rate at which the value of a currency reduces over time while the general prices for goods and services rise. The loss of value in said currency has less purchasing power than before. What someone could buy for $2 when their parents were teenagers is much less than what they can get for $2 now.

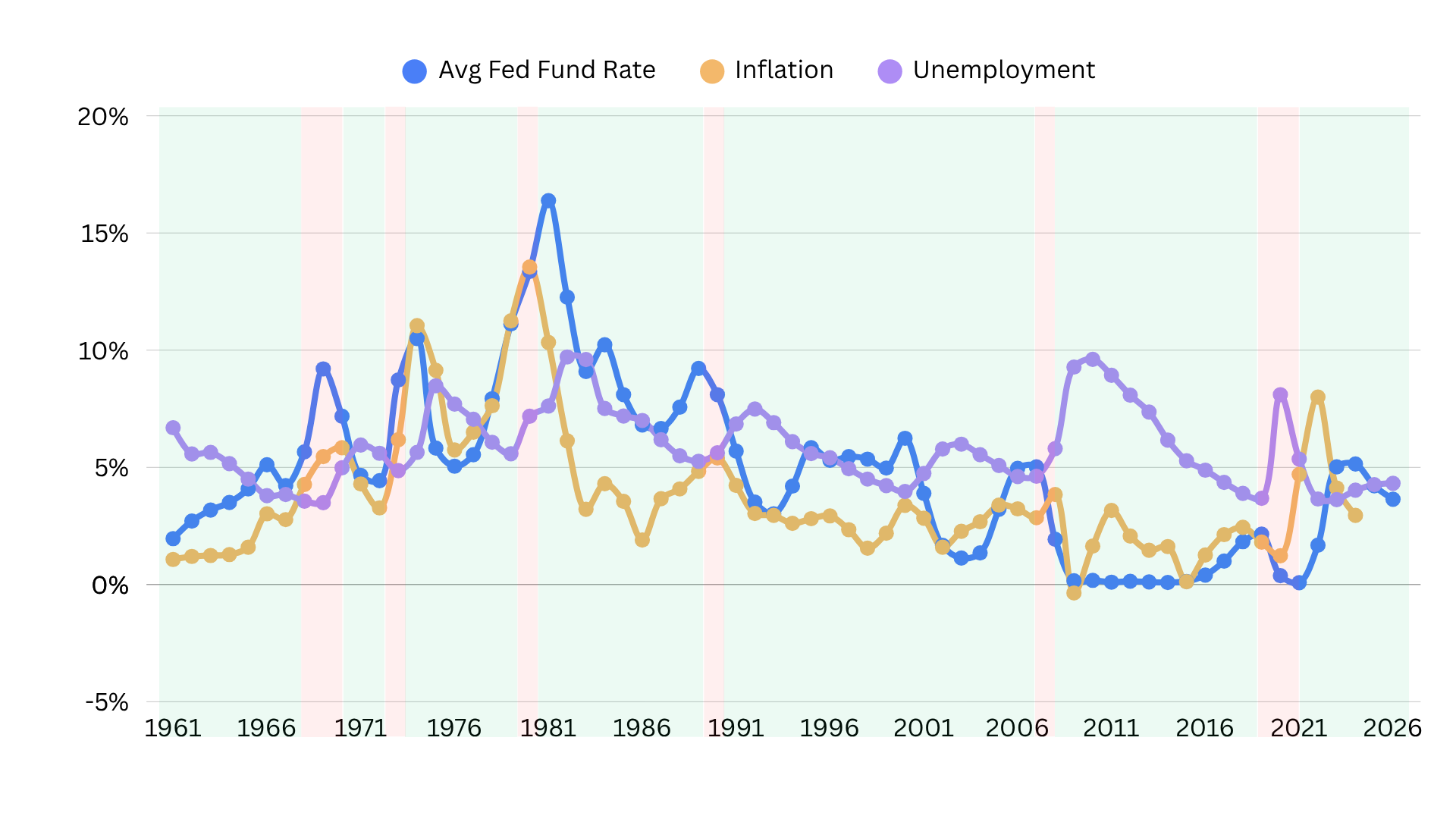

Every month, the Bureau of Labor Statistics(BLS) releases an updated version of the Consumer Price Index (CPI), which provides information on inflation and deflation. As a measure of inflation going back to 1913, the CPI also offers historical insight into economic growth.

Inflation cannot be stopped and gradually happens over time. This loss of purchasing power and price stability impacts the general cost of living, ultimately leading to a slowdown in economic growth and consumer spending. While interest rates are reduced and borrowing is made easier, earnings from savings accounts also decrease.

To combat this, a country's policymakers try to manage the supply of money and credit to keep inflation within limits to keep the economy running smoothly.

Types of inflation

The mechanisms of how the above drives inflation are usually classified into three types: demand-pull inflation, cost-push inflation, and built-in inflation.

● Demand-Pull inflation is when demand outpaces supply. The less available something is, the more expensive it becomes, and prices rise. With more and more people having disposable income, overall spending becomes higher, and increased demand affects the prices directly. It's the most common cause of inflation.

● Cost-Push inflation is caused by significant increases in the cost of essential goods or services where there is a lack of suitable alternatives or substitutes. Overall prices increase due to rises in the cost of wages and raw materials. Because the demand for the goods hasn't changed at all, it then falls on consumers to pay higher prices for finished goods.

● Built-In inflation happens when due to the expectation that inflation will continue, people require their wages to also increase in order to meet the rising costs due to said inflation. As workers need higher pay, not only does the cost of production overall increase, but so does the cost of living.

Understanding hyperinflation and deflation

The fact is, inflation isn't the only potential downside an economy can face.

While most economies can tolerate some inflation, a rapid surge in prices can result in hyperinflation. In this case, inflation is completely out of control. Not only do prices skyrocket, but inflation grows rapidly, usually by 50% per month. For context, the average annual inflation in the United States since 2011 has been 2% per year.

In the past, hyperinflation originated during periods of war, famine, and general instability. As access to food and fuel becomes limited, prices rise dramatically. Meanwhile, the cost of labor often remains the same. As hyperinflation continues, hoarding becomes commonplace and the economy comes to a standstill.

On the flip side, deflation is usually indicative of a recession or depression. While wages and prices tend to decrease, unemployment may rise, and economic growth stalls. Typically, deflation incurs when there is too much of a supply and little demand, or there is not enough money in circulation.

In addition, while credit tends to become more accessible during periods of inflation, deflation causes creditors to tighten their lending criteria.

Central banks usually step in with new monetary policies to reduce deflation. As prices plummet and unemployment gets widespread, deflation can be just as harmful as inflation.

What causes inflation?

One cause of inflation is a fiscal deficit, which is when governments spend more money than they receive from taxes and other revenues. This creates a large amount of debt over a period of time. The size of a country's fiscal deficit affects economic activity, growth, stability of prices, overall costs of production, and, of course, inflation itself. Fiscal deficit can lead directly to cost-push inflation.

The money supply is the total amount of currency held by the general public within a country. Inflation can also happen if a country's money supply increases more than the nation's economic output, even under normal economic circumstances for the country.

When there is more money in the public's hands purchasing the same number of goods, there is an increase in monetary demand, which causes firms to increase prices. Prices tend to only stay the same if the money supply increases at the same rate as economic output.

The labor market can also have an impact on inflation by influencing wage-setting and compensation practices that firms have with their employees. Companies can directly influence the price levels in the economy by changing the terms of contracts with employees and must cover the costs of their production. Therefore, if wages rise, the costs of their products will too.

So, how can we handle inflation to ensure our assets are continuously growing in value?

Protecting assets against inflation

Inflation can either be temporary or sustained, with sustained inflation being a period of continuously rising prices. Most inflation is temporary but still has effects on the economy.

So, how can we handle inflation to ensure our assets are continuously growing in value?

There are types of investments that increase in value during normal economic cycles, but the moment inflationary cycles begin, these investments start to decline in value.

A common strategy to attempt to protect against inflation is hedging, which attempts to limit risks in financial assets. Companies typically use inflation hedging to protect their investments from losing too much value during inflation periods.

One way to hedge investments is to purchase assets with a value that is usually directly tied to inflation. That way, should inflation rise, so will the value of their assets.

Another way is to invest in securities specifically designed to hedge against inflation. One suggestion for investors is to build a diverse and robust portfolio that is prepared to withstand and overcome multiple scenarios, including inflation.

What kinds of things can you invest in against inflation? Gold and other precious metals are usually the most commonly purchased assets here because these tend to often keep up with inflation. While you can't base your entire strategy on historical returns, the rise in gold and other metals prices has been consistent enough that it's a popular choice.

Recently, Bitcoin has been considered a potential inflation hedge because it's seen as being similar enough to gold in that it's limited, and thus less likely to be affected as much by inflation. However, this asset class is extremely volatile and investors can lose big.

Consider the Squid Game cryptocurrency, which had a price increase of 2,300% within a week. It went from $0.01 to $2,856 - a huge sum - and then crashed almost overnight. The developers of the currency made off with $3.38 million dollars in their scam, leaving investors and traders high and dry.

For those close to retirement age or individuals with a low-risk tolerance, participating in a such highly volatile market would be extremely stressful. In addition, given the lack of transparency around cryptocurrency ownerships and tools, it's important to be extremely cautious when researching this investment option. I do not recommend any cryptocurrency investments for my clients, due to its lack of stability and openness.

A more traditional option is to consider buying real assets, such as equities. They tend to represent the same businesses that influence both prices and wages, so they are more likely to reflect inflation in real-time and are far easier to manage.

At the end of the day, whenever you evaluate an investment, you need to consider inflation as a factor. Will the gains from your potential investment be greater than the loss in value due to inflation? Since the annual inflation rates are usually fairly stable, it's possible thoroughly estimate potential gains or losses for different investment scenarios.

Is inflation here to stay?

Inflation has always been here, but are these price pressures permanent?

For over a decade, the inflation rate has been around 2% annually. Over the past 12 months, the increase to 5.4% has startled many Americans as the cost of food and fuel has risen. However, another sign of sustaining, or long-lasting inflation, is the increased cost of labor.

Usually, labor costs exceed productivity in this case. But the exact opposite has been happening for years, with productivity being 3.5x greater than wages. Given that much of the current economic climate is powered by supply chain gaps, it's likely that the current inflation rate is temporary. As the labor market adjusts and the supply chain recovers, it's likely that prices will stall again as inflation decreases.