Maintaining generational wealth has never been easy—70% of wealthy families lose their wealth by the next generation. And 90% vanishes by the second one. Yet, with the current market challenges, many are choosing not to leave a legacy at all.

Wealth management advisors (such as myself) are likely noticing this trend.

Despite the vast amount of family wealth baby boomer parents amassed over the years, despite the trillions of dollars labeled for generational wealth transfer over the next 25 years, parents are leaving less to future generations.

Let's get a glimpse into the “great wealth transfer” and how inheritance prospects are shrinking.

The greatest generational wealth transfer in history…or is it?

According to Deloitte, $24 trillion will be transferred over the next 15 years to spouses or children. Most of it comes from baby boomers, the wealthiest generation in history. But this doesn’t necessarily translate into leaving a legacy.

For example, over half of Millennials believe they will inherit $350,000 or more from their aging parents. According to boomer respondents, their children are overestimating. Instead, the older generation plans to leave their children or grandchildren $250,000 or less.

In my own practice and when discussing with colleagues, I’ve found this pattern to hold true. Retirees have a completely different mindset than past generations regarding inheritance. Of course, they live in a vastly different world, too.

Why retirees are bypassing family legacy plans

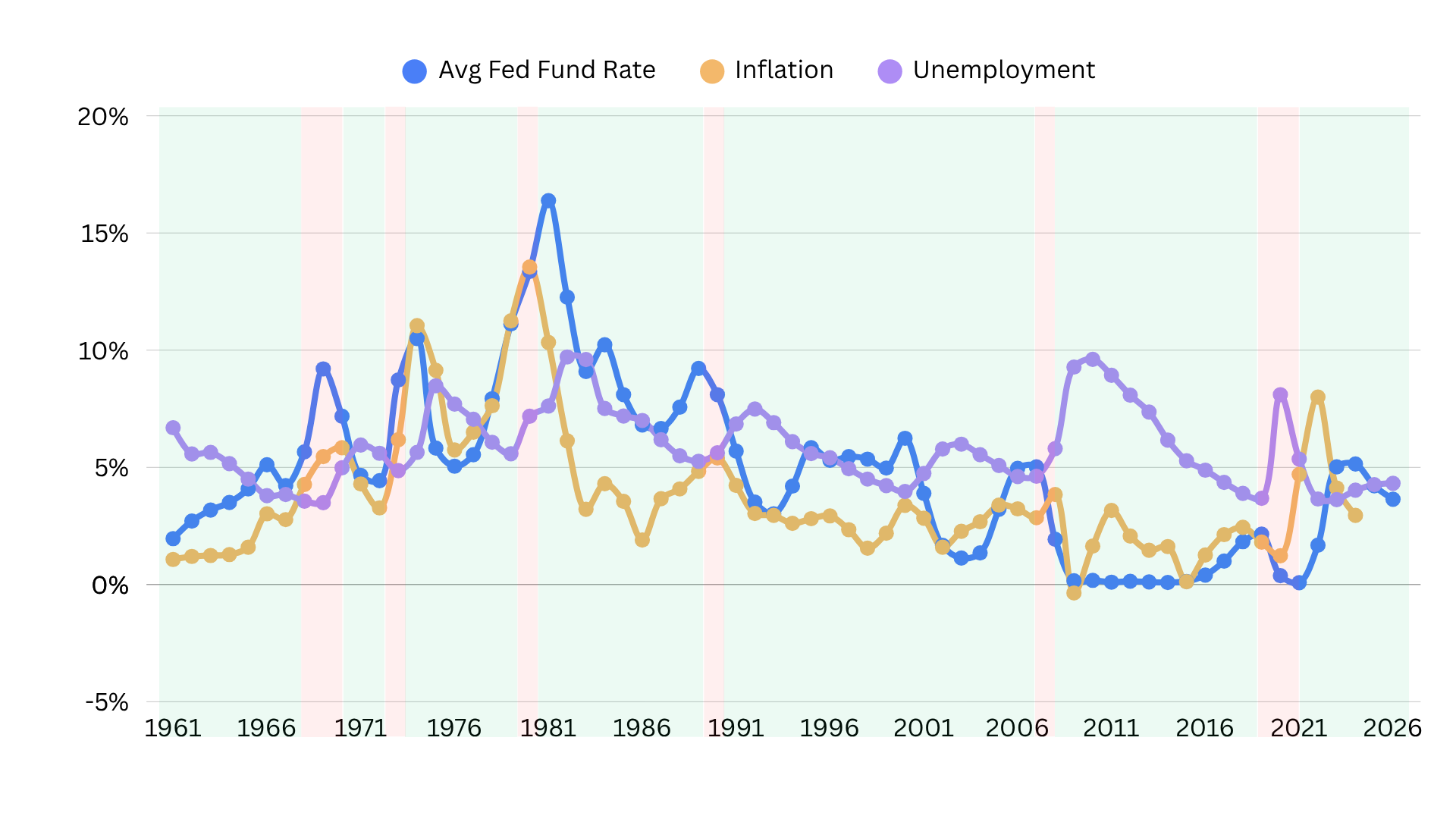

While baby boomers experienced a rapid rise in wealth, their later years have been far more tumultuous. Ballooning inflation, an unpredictable financial market, and murmurings of recession all contribute to spending anxiety for retirees. Baby boomers are also spending on their children—with 77% of Millennials and Gen Zers financially dependent on their parents.

Just as retirees attempt to stretch their funds further, the younger generation must cope with staggering student loan debt and a cost-prohibitive housing market. As a result, many families are spending their generational wealth now rather than passing it on.

The silent generation and baby boomers may not use all their savings within their lifetime, but many have other plans regarding what they leave behind. Rather than focusing on succession planning, retirees are looking at:

- Donating to a charity or preferred institution

- Creating a trust to support their pet

- Supporting children and grandchildren now

- Spending their wealth on personal bucket list items

- Keeping up with rising healthcare costs

What if you want to leave something to future generations?

Of course, there are individuals who want to leave at least some of their inherited wealth to their children. However, there are often concerns that the younger generation may blow through their inheritance.

Communication offers the best, direct solution. Including your loved ones in the financial planning process can build trust and enable you to help them understand the value of wealth management.

In addition, you can use a trust to your advantage. For example, you can use a trust fund to dole out the inheritance in small distributions over time. Or you can use a lifetime discretionary trust and place a trustee in charge of the inherited wealth. This trustee would then distribute the funds as required.

How younger generations can cope with a smaller inheritance?

While retirees are leaving less to their children, they aren’t taking everything with them. Generation X will likely get the most from their parents, receiving $29.6 trillion over the next 25 years. Millennials are expected to inherit $27 trillion in the same time frame. Although potentially, they will eventually surpass Gen X in terms of inheritance, uncertain economic conditions can greatly alter this outcome.

Regardless, it’s unlikely the younger generation can expect anything soon. So, what steps can they take to preserve and grow their own wealth? There are some general strategies:

- Have family meetings to discuss finances

- Develop an emergency fund

- Work with trustworthy financial and tax advisors

- Investment in long-term growth solutions—whether that be investments or career-based

- Reduce or eliminate debt

Want a second opinion?

Want some feedback

on your retirement plan? We can help.

With over 40+ years of experience in the financial sector, and as a licensed fiduciary, founder Jon Green can help you look over your retirement plan and understand whether you are on track.

You can book a complimentary session

or call me at +1 (828) 884-8840.