Healthcare premiums go up every year—and the additional costs have made healthcare a financial nightmare for millions of Americans attempting to save and preserve their wealth.

We’ve discussed the onset of for-profit healthcare monopolies and how they can affect your finances—often negatively. But large healthcare companies aren’t the only players buying up resources.

Private equity firms are just as invested in buying up organizations in the healthcare industry. And even though they can bring more profit, a healthcare system owned by private equity charges patients $400 more on average.

Today, we will talk about private equity and healthcare and how these acquisitions link to your financial goals and planning.

What’s the Big Deal with All These Buyouts?

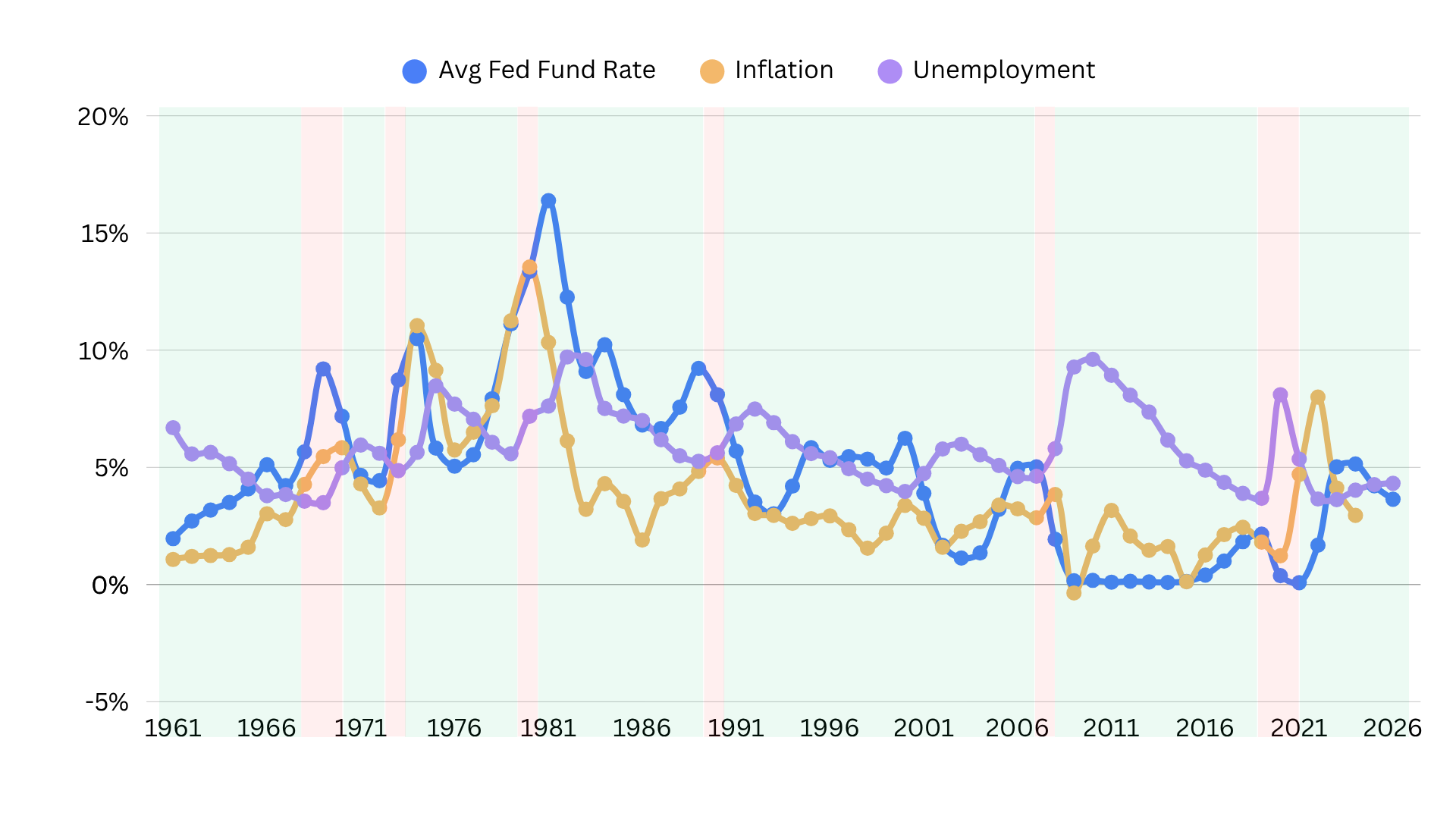

The early days of the pandemic revealed more about private equity’s role in the healthcare industry. Finance firms have bought out hospitals, clinics, hospital staffing agencies, nursing homes, hospice centers, and even ER beds. In 2018, over half of doctors were employees, not private practice owners. And over 70% of hospices are owned by private equity or for-profit firms.

Not only is this trend bound to get worse, but it has an adverse effect on doctors and care.

For example, in response to the coronavirus impacting profits, a private-equity-owned hospital cut staff benefits, reduced pay, and cut doctors’ hours.

Private equity firms state that they bring technology, innovation, and funds to healthcare providers. Yet we see, time and time again, a pattern of service reduction, price gouging, and doctor burnout.

And it’s important to note that throwing money at the problem of healthcare inefficiency is rarely the ideal solution.

According to a 2019 study from the California State Polytechnic University, private-equity-owned companies across industries have a 20% bankruptcy rate. When you compare this to the 2% rate held by publicly-traded organizations, we can see the vast risk in allowing these buy-outs.

Why such a high rate? Private equity often uses debt to acquire companies, and once the deal is complete, this debt is transferred to the new asset.

In other words, if Private Equity Firm A buys HealthCare First Hospital with a $50 million loan, the hospital is required to pay this off.

To then cut costs, these firms reduce services, workers, doctors’ hours, pay, benefits, and other hospital essentials to make HealthCare First Hospital profitable. Many of these equity-controlled healthcare providers also squeeze insurance companies through overvalued or surprise bills, thus driving up the cost of premiums. And that’s if they are affiliated with insurance—many are not.

And the icing on the cake is that these firms are also defrauding government programs by filing false claims. Meaning the taxpayers are footing the bill. Since 2013, the settlement amounts alone for 25 companies making false claims was $570 million.

This problem is compounded by the fact that these equity firms are becoming a dominant market. Starting in 2013, two private equity companies controlled 30% of the healthcare market.

Free Market or a Scam?

Private equity investors present their case as a way to maximize efficiency. In theory, they can better handle the hospital’s finances to reduce waste. They also claim to bring technological advancements, improve communication, and generate revenue.

The problem here is that private equity firms specialize in short-term profit. Most plan to sell their new assets within three to seven years with a goal of increasing profit by up to 30%.

These firms aren’t interested in fostering a sustainable, long-term business. And when they thrust debt onto their new acquisitions, they set healthcare organizations up to fail. And the patients? Who cares!

What consumers get are:

- Fewer hospitals, beds, and doctors

- Higher bills

- Higher premiums

- Longer wait times

- Smaller provider networks

- Taxes wasted on false claim allocations

In other words, individual investors like you and me are paying more for less. And eventually, as hospitals close, residents of rural areas and small towns may need to drive hours to reach their “local” specialists.

Many of these issues are similar to what we see in private healthcare monopolies. Except private equity plans to exit the business once it’s impossible to squeeze pennies out of these fatigued systems. As a result, these “assets” — our hospices, clinics, hospitals, and nursing homes—will be closed or sold to a for-profit healthcare system.

Private equity in healthcare, if left unchecked, is a liability for individual investors. Those looking to build wealth or retirement portfolios must reduce their savings to meet even basic healthcare needs. Meanwhile, those already in retirement and looking to conserve their funds may either run out of money or be unable to get access to healthcare.

What You Can Do

Until proper regulation is passed to prevent monopolies—whether they are private or private equity, most of us are on our own. For those looking to conserve capital and build wealth, it’s helpful to:

- Critically analyze health insurance plans to accommodate likely needs and limit spending

- Keep an updated list of in-network providers

- Live close to a metropolitan area with several healthcare facilities

- Work with private practices over private equity or HMO-owned facilities

- If your health insurance offers complimentary telehealth, try using it and see if it works for you

And, in terms of finances, you'll want to work with a trusted, fiduciary advisor who can help you navigate the retirement landscape.

Want a second opinion?

Want some feedback

on your retirement plan? We can help.

With over 40+ years of experience in the financial sector, and as a licensed fiduciary, founder Jon Green can help you look over your retirement plan and understand whether you are on track.

You can book a complimentary session

or call me at +1 (828) 884-8840.