By

Jon Green

November 30, 2020

When we look at the news, there are a lot of different rates thrown about. Half of the time, these various rates are just labelled under the umbrella term “Federal Reserve Interest Rate”. And this makes it confusing when you read two different articles and you find contradictory information.

But knowing how interest rates are set is important. They dictate how much profit we’ll get on a fixed-income investment, like a CD. Or how affordable it is to get a loan.

The Federal Reserve isn’t directly pulling the strings behind your bank’s lending rate. But it does affect both commercial lending and savings accounts.

So in this article, we’re going to discuss the key rates you need to know about.

What is the Federal Reserve Interest Rate?

The fact is, there are a few different interest rates that are affected by the Federal Reserve. To be specific, there is the Federal Funds Rate, the Prime Rate, and then there’s an entirely different rate for mortgage loan calculations.

You may find these terms thrown about, or simply combined under the term “Federal Reserve Interest Rate”. But to throw all of these rates under the same umbrella isn’t helpful. And it can make reading about changes in each individual rate confusing.

So let’s talk a little bit about what these specific rates are and how they affect you.

The Federal Funds Rate vs The Prime Rate

If you have kept up with the news recently, you may have noticed economists calling out the Federal Reserve for lowering its interbank rate in an attempt to control inflation.

The Federal Funds Rate is basically the rate at which the Federal Reserve will lend money to banks. Sometimes it’s called the Overnight Lending Rate.

Here’s how it works.

All banks have basic lending deposit requirements. Every day, they have to have a certain amount of cash on hand in order to cover deposits. But during the day, when money is being exchanged, banks don't know what they have. That's why they used to close at 2 o'clock - so they could count the money.

And at the end of the day, the bank is going to have to deposit whatever they have. And the Fed requires you to hold 25% of that in cash that night.

But what can banks do if they come up short?

They borrow that money from the Federal Reserve.

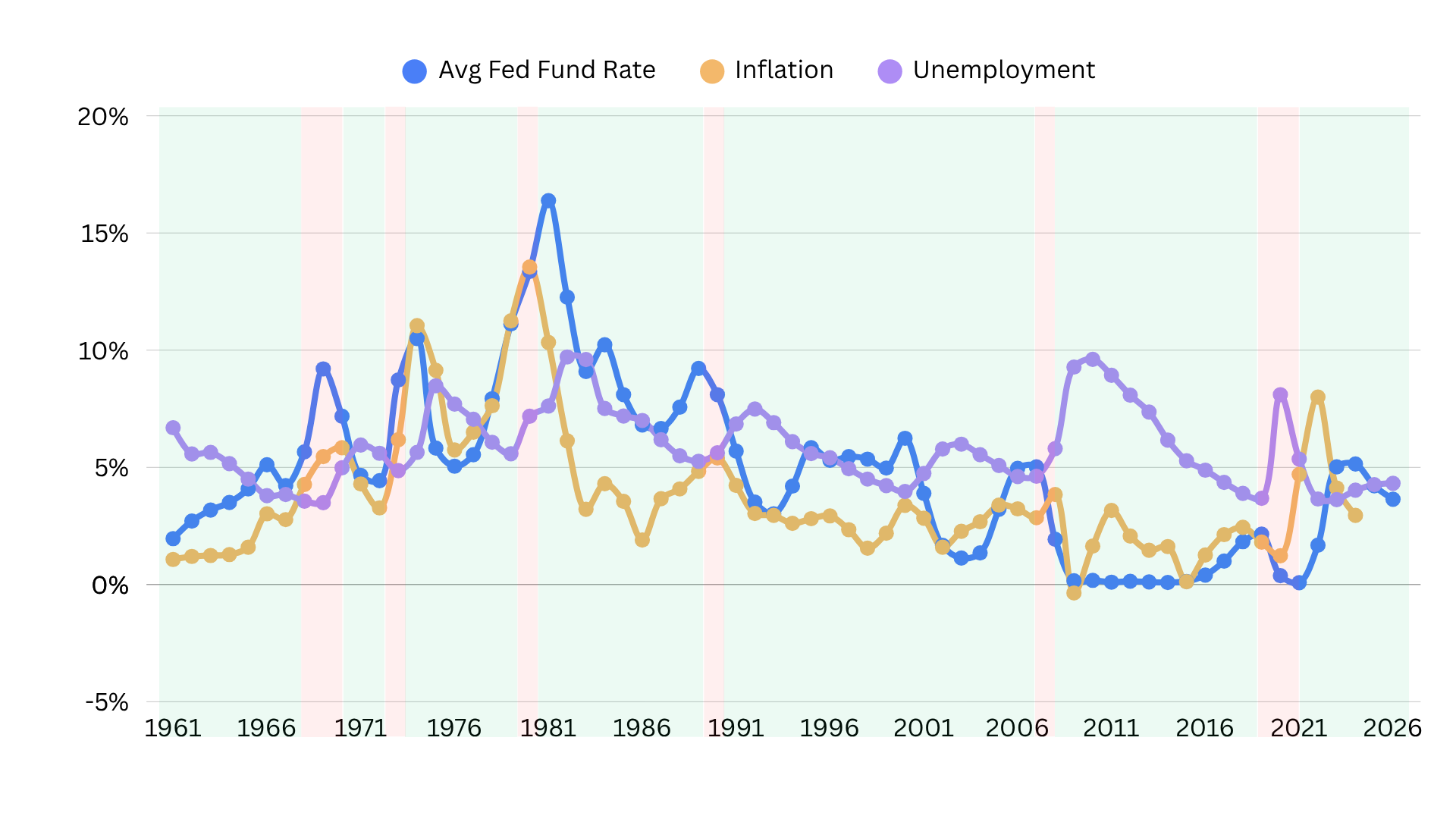

Right now, the rate is 0.25%. This is critical because that's what the banks are paying for the money. Banks can basically take out money at 0.25% and then they can go out and charge you 2-3% to use that money.

And while the bank does have to pay back the money they borrowed, they can also make a lot of money in 12 hours before it's paid back.

Because this is the rate the Federal Reserve uses to lend to banks, it is tied to other banking rates, like the Prime Rate.

The Prime Rate is what actually affects most of us directly. This rate is set by commercial banks and is used for both loans and savings accounts.

The reason it is so often conflated with the Federal Funds Rate is that the Funds Rate usually affects the commercial bankings rates.

Right now, the Federal Funds Rate is low, at 0.25%. And you’ll notice that most banks are offering low-interest rates on both their lines of credit and savings accounts. But once the Federal Funds Rate goes up, the Prime Rate probably will, too.

Another Criterion for Mortgage Rates

But mortgage rates are a little different. If the Federal Funds Rate or the Prime Rate go up, mortgage rates might stay the same.

That’s because the first two rates are based on a short-term timeline - a couple of years max. Your mortgage rate, however, is based on a 15 to 30-year time span. That means it has to build inflation into its calculations.

Let's just say I come to you and borrow a million dollars over 30 years. The Prime Rate is 5%.

You probably won’t give me the Prime Rate. In fact, it’s more likely you would charge close to 8%. That’s because, over time, inflation is going to take place. And if you charge 5% over 30 years and inflation is 3%, your return is only 2%.

How does a low Fed Funds Rate affect you?

So, we’ve covered the Federal Funds Rate in-depth, and we know it affects our wallets indirectly through the Prime Rate.

The Federal Funds Rate basically offers a starting point for banks to lend their money to you. The lower the Fund Rate, the lower loans and CD interest rates will be.

And that’s where we are right now. Since the Federal Funds Rate is low, we’re seeing cheap credit and almost stagnant fixed-income savings options.

While this will stave off inflation - which is the primary reason for lowering the Funds Rate - it has other downsides. Credit may be more affordable, but accessibility is still determined through an individual’s creditworthiness. Even with the introduction of alternative data, banks ultimately decide who is eligible for a loan - and most are risk-averse. This means thousands of creditworthy individuals won’t be able to take advantage of the cheap capital.

So that’s one issue. But what if you don’t need credit, you just want to build your wealth and plan your portfolio?

If banks are charging you 2-3% for a loan, they may be offering 1% or less on savings schemes. The low-interest-rate makes fixed-income options like bonds or CDs less appealing unless you have a big chunk of change you can leave in the bank for a year or two.

Consider this, even if you get a 1% on the savings of $200,000, you’ll only make $2000 a year.

This tends to push investors more towards riskier options - like the stock market - to find adequate returns.

In other words, a low Federal Funds Rate:

- Disincentives fixed-income assets and savings options

- Encourages borrowing

Why can’t banks offer more?

When it comes to pricing, commercial banks won’t make money if they offer a better interest rate for CDs compared to their loan rate. That’s why lines of credit will always take more interest than a saving account gives.

Competition between banks is another factor. Even if a bank wanted to raise rates on their CDs or other fixed-income assets, they cannot get too close to their lending rate. And they can’t raise their lending rate too high, as they also want to offer more competitive rates to attract more customers.

Because of this, you’ll find most banks sticking only a few points above the Federal Funds Rate.

Want a second opinion?

Want some feedback

on your retirement plan? We can help.

With over 40+ years of experience in the financial sector, and as a licensed fiduciary, founder Jon Green can help you look over your retirement plan and understand whether you are on track.

You can book a complimentary session

or call me at +1 (828) 884-8840.