Yet so much of the language we use to discuss portfolio construction deals with variable income - particularly the stock market. Phrases like buy low, sell high, timing the market, and bull runs are far easier to recognize than duration, and convexity. Interest rates are rising? Which interest rates?

The process isn't like the stock market when it comes to investing in fixed-income assets. For that reason, it's critical to understand how the fixed income market works and strategies are out there.

What is fixed-income?

A fixed-income investment, also called an asset or instrument, is a group of asset classes that is meant to help individual investors create a steady source of income. The most well-known fixed income product is the bond, but that isn't the only kind of fixed income security. Outside of the various types of bonds, there are certificates of deposit (CD), fixed-income mutual funds, and asset allocation ETFs.

So, how does fixed income investing work? Let's stick with bonds for a moment.

A bond is focused on preserving capital and income. A borrower, usually a company or the government, makes payments to a third-party investor of a fixed amount including interest on a consistent schedule until the fixed income security matures. Once the bond reaches maturity, they pay the remaining principal amount to the investor. Payments are typically coupon payments on bond holdings and are exempt from taxes.

Many bonds also have legal protection to them that other equity securities such as shares or stocks don’t.

Let’s say- heaven forbid- the worst-case scenario happens and a bond issuer goes bankrupt. If that were to happen, the bondholders would be repaid via compensation when assets are liquidated. Meanwhile, if the same scenario happens with stocks, shareholders often don’t see a penny. However, this doesn't mean a bond owner will necessarily recover their income.

Bonds and other fixed-income assets aren't "risk-free." But the level of risk can usually be estimated by the type of investment.

Types of fixed-income instruments

A fixed-income portfolio can contain a variety of products. The most well-known are government or corporate bonds. But there are many other types, each with its own investment grade, pros, and cons. Let's go over them:

- Treasury Bills, Notes, and Bonds - These not only have the aforementioned regularly scheduled payments of acquired interest (a.k.a. “coupons”) but they also come in a variety of maturities. Some mature in just four weeks while others can take as long as 30 years. These are considered the safest form of bonds when it comes to risk.

- Municipal Bonds - State, city, and county governments offer bonds called municipal bonds. They carry a higher risk than Treasury bonds but are still considered more secure.

- Corporate Bonds - There are various types of corporate bonds, and the rates entirely depend on the organization's financial ability. Corporate bonds with higher credit ratings, which suggest a greater likelihood of regular payouts, typically offer a lower coupon rate. Keep in mind that economic setbacks can result in a major loss of value and you may not see any return if you end up getting bonds from the wrong company.

- Junk Bonds - Corporate bonds with low credit ratings are generally labeled as junk bonds due to the high likelihood of default. These bonds are risky, even if they advertise themselves as high-yield bonds.

- Certificate of Deposit (CD) - This fixed income investment has a set interest rate over their entire term, typically starting out at increments of three months to a year before increasing to two, three, and even five-year terms. You can very easily acquire these at banks or credit unions, and they’re an alternative to putting money in a savings account.

- Fixed-Income Mutual Funds and ETFs- If you don't mind shouldering a higher management fee, there are mutual funds and ETFs that focus on fixed-income investments.

Why invest in fixed-income?

Like any type of investment, fixed-income has its own advantages and risks. Generally considered more stable, so long as you stay away from junk bonds, investors can count on regular income from their fixed-income assets. During periods of extreme volatility, regular income streams can provide some peace of mind.

Fixed-income investments primarily help preserve capital. They are much more predictable when it comes to knowing how much return you’ll get, and they may provide a premium above inflation. When you only include bond issuers you trust in your portfolio construction, then weathering a long-term strategy becomes less stressful.

Furthermore, while bonds rarely offer as much growth as other asset classes, Treasury and Municipal Bonds are relatively less risky than betting on individual stocks. The return is guaranteed, but you might not turn over as high of one as you would’ve liked.

However, slow growth can be offset by potential tax benefits. For example, interest income from U.S. Treasury bonds is exempt from both state and local income taxes. Likewise, the interest income you receive from municipal bonds is not subject to federal taxes.

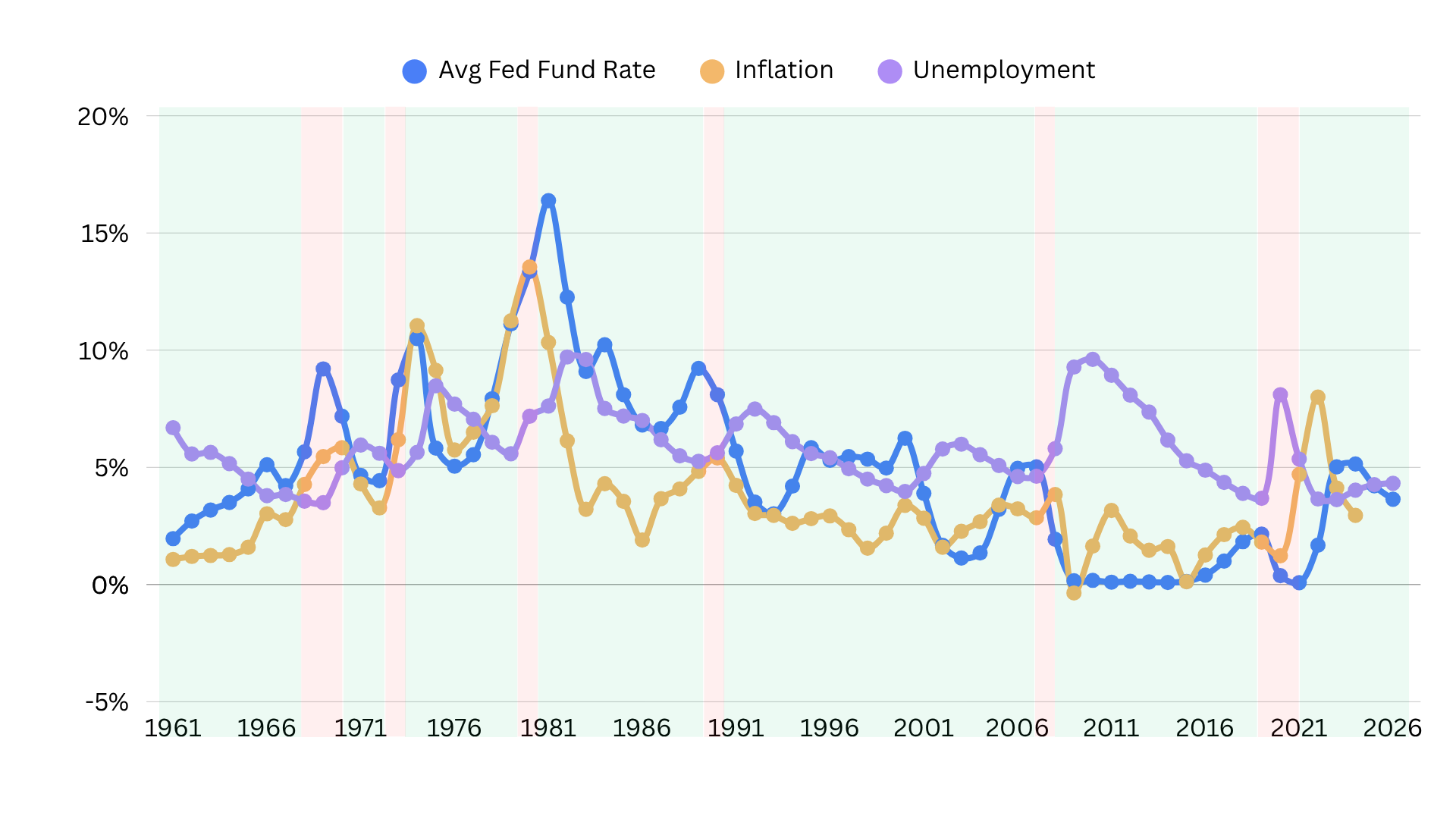

The major concern the individual investor might have is the rise and fall of interest rates. This is because:

- When the Federal Reserve increases the Federal Reserve Funds rate, bond prices drop.

- When the Federal Reserve Fund rate decreases, bond prices increase.

What does this mean for fixed income investing and strategy? If interest rates rise, investors run the risk of being locked into lower-interest bonds until maturity, or they lose their principal if they try to sell. This is why an entire portfolio of fixed income investments can become a hassle.

However, so long as you trust the bond issuer and the bond does not default, an individual investor who keeps their low-interest bond does not necessarily lose money. This is because they will receive their principal when the bond matures.

The other downside of a fixed-income-based portfolio is inflation. If inflation outpaces the bond interest rate, then an investor can lose out as their money loses value. For that reason, it's typical for an investment strategy to retain a percentage of its asset allocation in other asset classes.

Want a second opinion?

Want some feedback

on your retirement plan? We can help.

With over 40+ years of experience in the financial sector, and as a licensed fiduciary, founder Jon Green can help you look over your retirement plan and understand whether you are on track.

You can book a complimentary session

or call me at +1 (828) 884-8840.