With experts arguing about whether we are recovering, in a depression, or entering a recession, the economy is even more confusing. None of these are a collapse. A total economic collapse is unprecedented in our history, with the closest reference being the Great Depression.

That begs the question: What would cause a collapse, and how could it influence our wallets and portfolios?

In this article, we’ll explore the concept of an economic crash, potential tipping points, and potential economic consequences of a collapse. We’ll also review some tips on preparing an emergency plan, particularly for something longer than a recession.

How to Define Economic Collapse

An economic collapse is a complete breakdown of the market and economy. This event is not a bearish trend or a recession—it goes far beyond the normal crisis. There are minimal safeguards for financial institutions and governments to combat such a reality. Furthermore, the dismantling of primary financial instructions or the national government can trigger or exacerbate a collapse.

The United States has never suffered a complete collapse—although the Great Depression teetered on the edge of ruin.

One of the most well-known examples of an economic collapse is the Weimar Republic in Germany in the 1920s. A combination of depleted funds and expected WWI reparations left the German government in a lurch. It could not raise enough money to pay the debt. And thus, it began printing money. This action led to hyperinflation, bankruptcy for millions of Germans, and a lack of law and order.

The economic stagnation and subsequent collapse of the Soviet Union in the 1980s and 90s led to a complete breakdown of not just the economy but the government.

Even today, we can look to Zimbabwe and Venezuela for examples of extreme hyperinflation and dysfunctional economies.

Collapse vs Crisis

As we can see, a collapse often includes a complete societal breakdown—with many governments unable to recover.

A crisis, however, may be reversed and often does not include absolute market failure. It could be said that a crisis is the last step before a collapse, which may be why it can be difficult to determine which event counts as a crisis or collapse.

The Great Depression, for example, may be labeled as either one, depending on who you speak to. This period was not only the longest economic downturn in United States history, but its effects had a ripple effect across the globe. System weaknesses, poor policy, and the stock market crash compounded to throw millions of Americans into poverty.

Events significant crises were the 2008 Financial Crisis and the Greek Government-debt Crisis. Without timely intervention, these events might have snowballed into a full collapse.

Potential Tipping Points

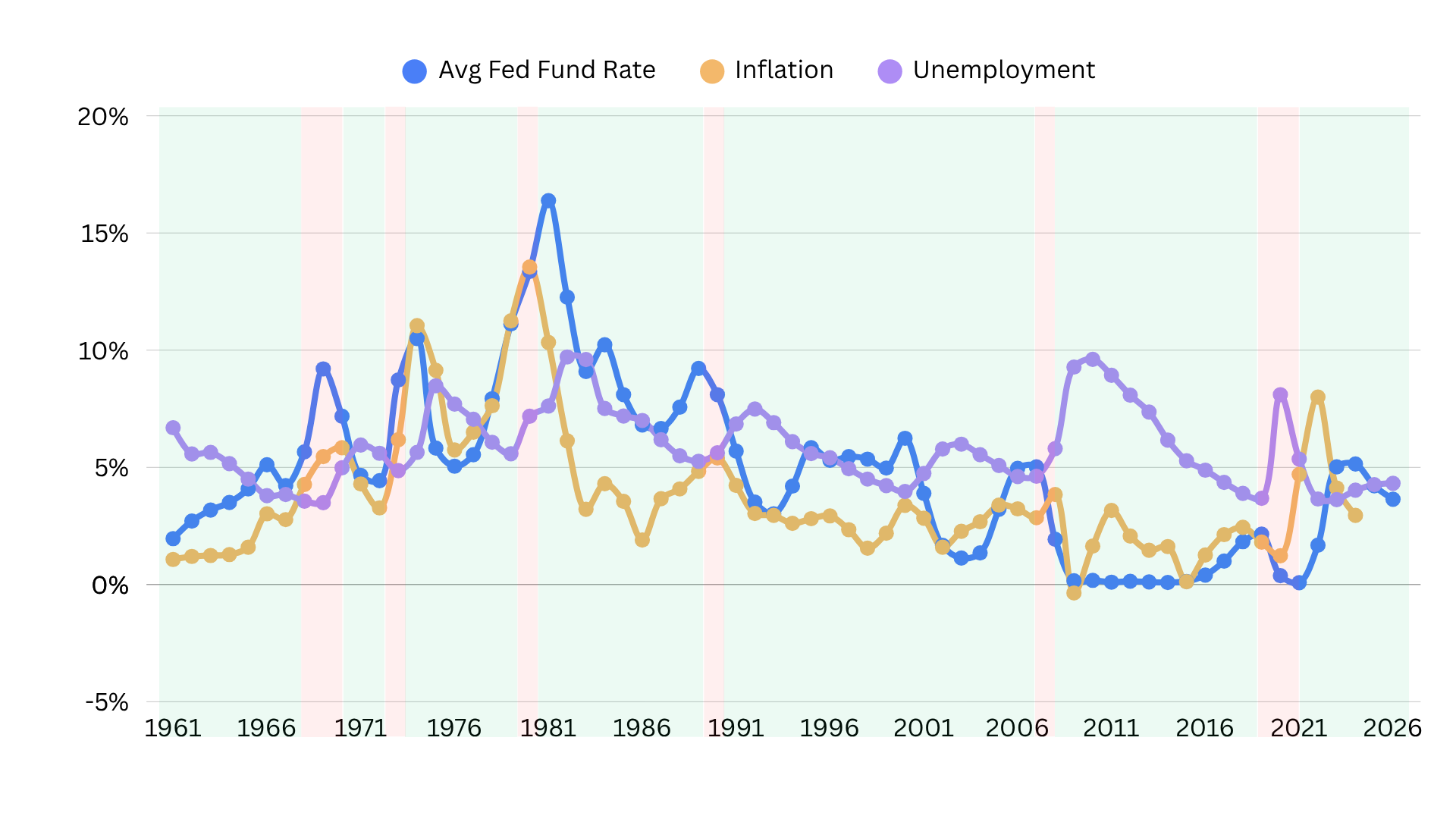

The US economy appears to be doing well, according to an IPC economic outlook report. In fact, by the end of 2023, unemployment dropped to 3.8%, and inflation continued to decrease. The markets appear to have stabilized.

But that’s not the whole story.

The financial markets have long been removed from the realities of the American economy. Stock prices rise and fall based on investor emotion, not asset quality. Checkr, a background check and verification company, surveyed 3,000 workers and managers to discover that employees are overworked and underpaid. More and more Americans are taking a second job to pay the bills.

Housing continues to be cost-prohibitive for millions of Americans, many struggling with inflation and price gouging. Private equity has bought a sustainable amount of resources, such as hospitals, clinics, housing, and advisory firms.

In other words, the economy hasn’t necessarily healed just because the numbers look a little higher than a few months ago. One catastrophic event might be enough to drive the economy into a downturn.

Below are some potential tipping points:

- Debt Limit

Republican representatives use the debt ceiling as a bargaining chip when setting the national budget. However, each threat of default has become more and more a genuine risk.

This begs the question: What happens if the US doesn’t pay its bills?

While this has never happened in the country’s history, it’s clear that defaulting will weaken the US economy and affect the global markets. The complete scope depends heavily on which bills aren’t paid—but it’s likely that the economy could fall into a recession.

Typically, defaulting may lead to increased public debt, lower employment, fewer taxes collected, increased financial market regulation, currency devaluation, and strict austerity measures. All of these consequences often lead to civil unrest and potential changes in government. The nation may also face reputational damage, which can limit access to potential credit sources, trade deals, and other economic activities.

- The 2024 Election

The January 6th Insurrection revealed the deep division in the political realm. Tension over the future of the country is at an all-time high.

Regardless of who wins in the upcoming 2024 election, the American people are facing significant dysfunction.

However, there is a new potential policy that could further break down the current system. Literally.

Some politicians voicing their desire to dismantle the federal government have advocated for a new approach, Project 2025: The Presidential Transition Project.

Project 2025

One of the top concerns many voters have—on both sides of the aisle—is the conservative initiative Project 2025. This project centers around implementing hundreds of policies severely restricting the federal government. In most cases, the recommendations greatly reduce or eliminate every federal department.

Let’s take the Federal Reserve, for example. According to the Project 2025 Playbook, the next conservative president (or any elected official) should advocate for free banking. Free banking would prevent the federal government from setting interest rates or supplying money—essentially abolishing the program. This would introduce unprecedented chaos into the already unstable economy.

Other potential policies include removing environmental, social, and governance (ESG) factors from the department’s guidelines, thus eliminating a framework meant to uphold sustainability.

The Small Business Administration (SBA) would also face significant cuts. The plan is to directly cut the direct lending program for small businesses and instead redirect them to private lenders. If a policy such as free banking is implemented, small businesses must contend with lenders who can freely set their interest rates—if approved.

Numerous policy recommendations throughout the playbook, many of which will have significant economic ramifications—and could qualify as significant government disruption. All of which could lead to a collapse.

- Geopolitical Conflicts

The number of geopolitical risks across the world is only growing. At the time of writing, these are some significant conflicts:

- Israel’s bombardment of Gaza and additional skirmishes in Lebanon, Syria, and the Red Sea

- Russia’s continued war against Ukraine

- Azerbaijan’s invasion of Armenia

- War in Sudan

These are just a few of the violent conflicts that exist and exclude factors like climate change, forced migration, local elections, and other potential events.

Geopolitical events affect our trade agreements, the world’s supply chain, and government spending. High tensions and conflict make everything from tourism to business and international peace-keeping difficult.

- Fluctuating Inflation (and Price Gouging)

Fluctuating inflation—or price gouging, which is just as relevant—reduces purchasing power for the everyday American. It devalues portfolio value and reduces overall spending. Less spending results in a stagnant economy, leading to fewer jobs and more economic unrest.

While this may not cause collapse, it may lead to other tipping points.

- Low Bank Liquidity

Under high-interest rates and little regulation, many banks are facing low liquidity. This means their profit margins are shrinking, and overborrowing can quickly lead to a bank crash.

If more banks fail, we will likely see increased public panic and less spending. While policies are in place to prevent a run on the bank, every loss significantly impacts depositors and the Federal Reserve’s ability to answer a crisis.

Potential Economic Consequences

So, what’s the worst that could happen? While we can’t say for certain—there are too many unknown variables at this point and time—there are some consequences that often follow economic discontent and collapse.

- Hyperinflation

The greatest worry most have is hyperinflation. This occurs when inflation rises rapidly each month, with the percentage rise being as high as 50% or more. Post-WWI Germany is a good example of hyperinflation.

Another recent case is Venezuela. While the country has experienced double-digit inflation rates since the early 80s, poor government policies and socioeconomic stressors transformed regular inflation into hyperinflation. The ongoing political crisis and several policies, including evaluating the bolívar and lowering the minimum wage, led to inflation rates as high as 1,000,000%.

Ultimately, hyperinflation leads to individuals being unable to buy anything. As prices eventually come down, so do wages, leading to an economic depression.

- Depression

Economic collapse could lead to a full-scale depression—few jobs and little pay. While there are many examples of an economic depression, the collapse of the Soviet Union in the 1990s highlights what an economic collapse could mean.

Poverty in the Post Soviet States increased 10x. Russia’s GDP was halved. Smaller states also saw their GDP plummet; some, such as Georgia, Kosovo, and Tajikistan, never recovered. The economic chaos also facilitates a rise in organized crime, mass migration, and extensive poverty.

- More Bank Failures

It’s perfectly possible that an economic collapse—especially those under Project 2025—could lead to a complete collapse of the banking system. With many Americans using credit cards and payment methods, this could mean being locked out of their accounts.

An increase in bank failures leads to further investor distrust of the economy. Even if the situation can be controlled, losing faith in the financial system and currency can lend itself to additional problems. Banks considered stable may go under if a panic ensues.

- Currency Devaluation

Another significant consequence of economic collapse is that currencies are devalued. This can lead to hyperinflation or a currency crisis, further devaluing money—namely, the U.S. Dollar.

It also further devalues the currency. If hyperinflation were to devalue the U.S. Dollar, the currency would become less favorable worldwide. Investors at home and abroad may prefer to trade in another, more stable currency. In other words, the US Dollar would no longer be the world standard in the international market.

- Lopsided International Agreements

With an unstable economy, fewer countries may be willing to sign new trade agreements. Furthermore, increased economic stressors at home may result in officials signing deals that are not beneficial to Americans.

As an economic powerhouse and superpower, the United States has been able to successfully advocate for its interests abroad, whether that be in diplomatic missions or trade agreements. If an economic collapse leads to a depression, currency devaluation, or other ills, our government may have less leverage in future deals.

- Lack of Infrastructure

An absent economy translates into less spending, not just for people but for the government. Infrastructure projects will likely remain stagnant. Depending on how long it takes for the economy to bounce back and the effects of the collapse, funds on a state and federal level will be incredibly limited. As a result, money will likely be used only for emergencies or immediate needs—not on improving or repairing infrastructure.

Furthermore, as climate change continues to fuel natural disasters worldwide, not to mention changes in flora, fauna, and resources, the government may not have the agility or financing to respond effectively.

What Could This Look Like in Reality?

It’s entirely possible—although unlikely—that none of the above consequences occur under an economic collapse. In addition, many of these consequences wouldn’t necessarily happen immediately.

The most perilous aspect for many Americans will be maintaining their long-term financial commitments. To better illustrate what I mean, here are a few concrete examples of how ordinary decisions can derail financial stability in a crisis:

Example 1: Building a Home.

Consider that you are planning to build your dream home for retirement. You have bought the land, signed a contract with a builder, and sold your current home to pay for the construction. Unfortunately, the economy crashes. The disaster has severely impacted the value of the US dollar.

The devaluation of the currency, combined with spreading geopolitical conflicts, leads to a supply chain disruption. The builder cannot get the materials to continue working even though. you’ve already advanced the contractor thousands of dollars. You’ve also sold your home and are living in a rental.

As panic and further disruption sets in, inflation begins to rise again. You have an emergency fund—but now everything costs more, and you have no idea when your home will be finished.

To preserve government funds for core services, the government makes several cuts to the budget, including SBA programs and loans. This hits small businesses hard as they struggle to maintain cash flow.

After nearly a year and a half of sporadic delays, your house is 70% completed. However, the contractor is unable to sustain his business. Materials are too expensive, few will agree to price increases, and there is a labor shortage. The company is unable to get a loan. You must now find another builder.

Example 2: Your Child’s College Education.

You’ve saved for over a decade to help support your daughter obtain a degree. She is doing everything “right.” She has a stellar GPA, has been a leader in after-school activities, and has received private scholarships from her ideal university—a public college.

However, even before the collapse she is missing opportunities. Previous scholarships and grants for women in STEM have been rescinded for public institutions, as they are now considered discriminatory against men. State funding has dwindled over the past decade—all public universities in your state now only receive 15% of state funding.

Furthermore, she is not eligible for federal student loans or grants—your income is too high. Because of the transition to free banking, interest rates are everywhere. The only interest rate she can get, even with you as a co-signer, is 25%. The loan would start accumulating interest after the first 6 months.

Your daughter plans to get a job, so that will help, even if it only pays minimum wage. And even if it’s a bad deal, your daughter is planning on a high-paying practical career. It’ll be worth it.

However, over the next two years, economic instability due to high interest rates, supply chain disruptions, a lack of regulatory safeguards, and a rise in unemployment has caused a downward spiral for banks. Your bank fails—and you are unable to access your cash.

Luckily, you have an emergency fund in cash, an account at another bank, and one at a brokerage. That softens the blow. However, you are unable to support your daughter’s education. And because of low bank liquidity, she is unable to get a loan for her tuition fees.

She drops out, unsure of when she’ll have the opportunity to return. As she does not have an engineering degree, she is stuck in a minimum-wage job—unless she is laid off as the recession deepens.

Example 3: Starting a Business.

You’re entrepreneurial. You’ve started two businesses in the past, and although you’re in retirement, you have an idea for a new venture. Your business plan is solid. You have trusted investors and friends who are on board with your idea. You’ve taken out a small loan to create a prototype product and get some initial marketing exposure.

You aren’t worried about paying back your loan or your investors. You have money to pay most of it back in the worst-case scenario.

In an economic crash, you are suddenly faced with a number of challenges. Consumers are buying less, and sticking with cheaper products they know rather than trying a new one. Prices for materials rise from inflation, supply chain issues, and perhaps even price gouging. You have to shift to cheaper materials, which makes your product less appealing to a shrinking consumer base.

What would have been a slam-dunk business in a regular economy is floundering. Your wallet is feeling the strain on your personal budget. And your investors are beginning to ask about their money.

Unable to secure another loan six months into the crash, you decide to fold the project. You can pay off the loan and most of your investors. But it left a significant dent in your retirement account. You have less money than when you started, with no way to know whether you’ll make it back.

To make matters worse, the federal government defaulted on the national debt. This has led to currency devaluation, thus causing your portfolio to lose value.

Aren’t These Scenarios Hyperbole?

Because we don’t know what the economic crash would look like or what policies would be in place, it’s impossible to determine exact scenarios.

However, our daily lives are intrinsically linked to our monetary policies. What happens at that higher level has a ripple effect. Without prompt and reasonable actions from our leadership, these issues tend to compound.

And there are several hidden effects beyond our financial stability. Personal safety, access to healthcare, clean public spaces, insurance coverage, and career opportunities are just a few aspects of our daily lives that can be negatively impacted. What we depend on today may not be there tomorrow.

Like with investing, once an asset loses value, it requires even higher gains to be actually profitable. A slide into an economic crisis or collapse will require more funds and support to heal.

Hoping for the Best, Preparing for the Worst

It’s possible we can avoid a complete economic collapse. After all, many variables affect the markets, and a single shift in geopolitics or fiscal policies can avert disaster.

However, it can be prudent to have an emergency plan. Emergency plans can be useful for any unforeseen event, like losing a job, getting a divorce, or experiencing a natural disaster. Some ideas for safeguarding financial security and mental health can include:

- Extend your emergency fund from 3-6 months to a year

- Keep a portion of your emergency fund in cash

- Avoid banks (as they can fail) and rather use cash management accounts through brokerage

- Reduce fixed expenses

- Diversify your asset classes

- Diversify income

- Be cautious about long-term financial commitments

- Include international investments in your portfolio

- Consider buying another stable currency, such as the British Pound or the Euro

- Minimize debt

- Maintain an emergency kit that includes life essentials, such as clothes, food, and medical supplies

- Nurture your support network

You may never need your emergency plan. But it never hurts to be prepared. At the very least, a backup plan provides peace of mind, so you can focus on what you love in the present.