By

Jon Green

March 28, 2024

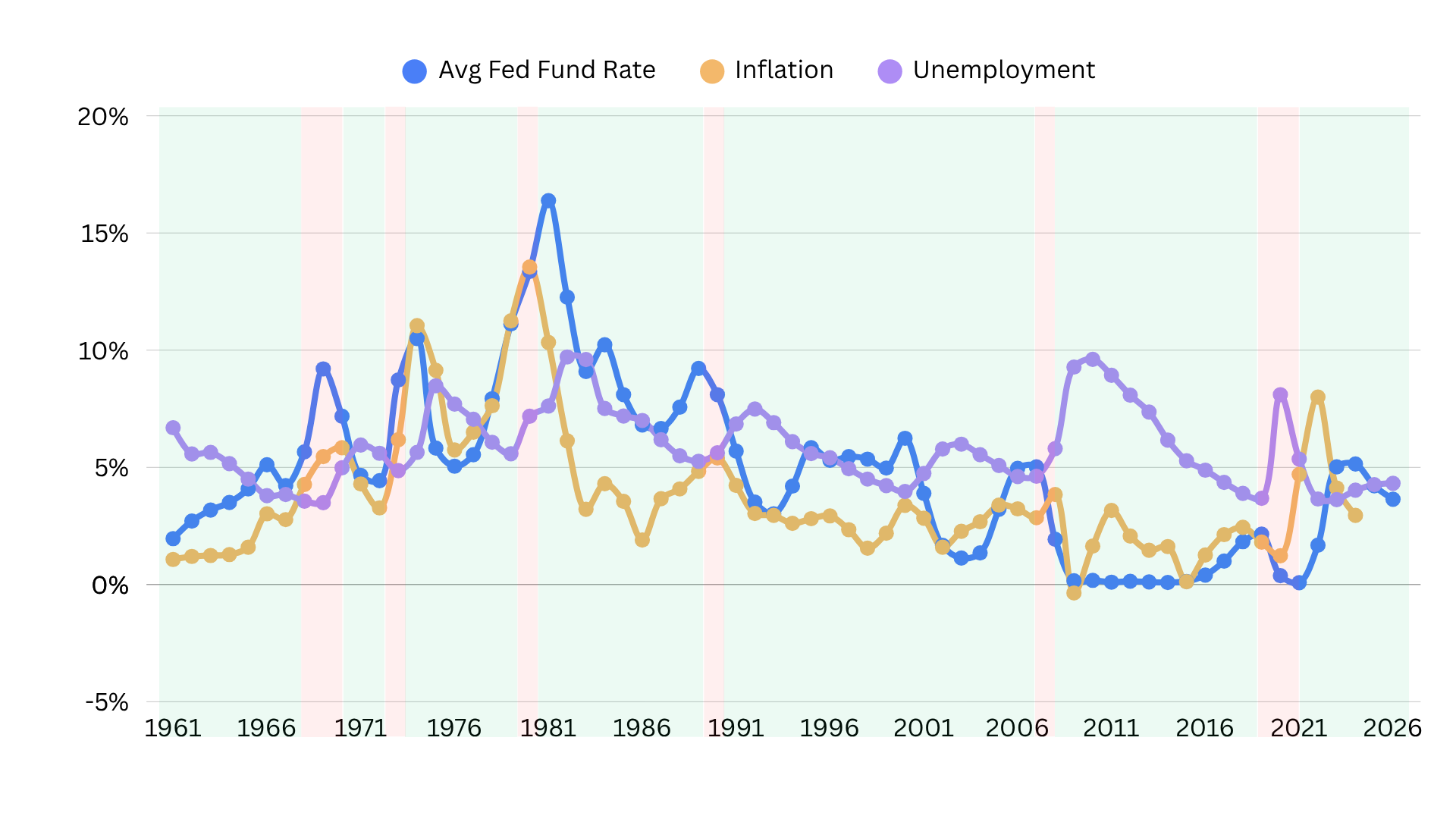

Economic stability affects an investor’s ability to preserve and grow wealth—which is why so many analysts are focused on recession forecasts. But, as is the case today, recessions aren’t easy to predict.

Currently, experts remain conflicted about the future of the domestic economy.

We took the liberty of researching what different experts are saying and summarizing why they think a recession is imminent (or non-existent).

What Experts are Saying

Yes, We’re in or about to Fall into a Recession

President and Chief Economist & Strategist of Rosenberg Research & Associates Inc., David Rosenberg, stated in a recent interview that there is a 85% chance that the US economy will enter a recession in 2024. To arrive at this conclusion, Rosenberg uses an economic model that uses financial conditions indexes, debt-service ratio, foreign term spreads, and yield curve data to calculate the state of the economy.

Senior Economist at Wells Fargo, Charlie Doughtery, believes that the Fed’s rate cuts may trigger a mild recession. TD Securities also expects a mild recession in 2024, suggesting that labor markets will weaken and government shutdown risks may negatively impact the economy.

No, We’re in the Clear

However, there are many experts that believe the US has averted disaster.

The first indicator that we aren’t in a recession is the fact that the National Bureau of Economic Research (NBER) has yet to announce one. This leading economic research organization offers thorough analyses and will announce potential downturns. The NBER last announced a recession in 2020, but no new forecast has been made about the 2024 economy.

According to the February National Association of Business Economics (NABE) survey, only 25% of business economists think the U.S. will face a recession. In other words, 75% believe the economy will recover. That said, there are points of concern—namely, political instability at home and abroad. The 2024 presidential election and continuing geopolitical conflicts could disrupt a recovering economy.

The business research group, the Conference Board, had also been warning of a recession for years, only to call it off this month. While growth remains largely stagnant, the firm believes that a surging stock market, low unemployment, potential credit availability, and increases in manufacturing orders all contribute to a more optimistic outlook.

Deutsche Bank also no longer believes that the U.S. is headed towards a recession due to resilient growth in the face of Fed interest rate hikes.

There’s No Way to Know for Sure

For a Wealth Management firm, U.S. Bank, the answer isn’t clearcut. Consumer spending fueled growth in 2023, which likely staved off a recession. That momentum has slowed—but that doesn’t mean there’s a downturn on the horizon. Lower inflation rates and a strong jobs market are just a few of the positive indicators keeping the market afloat.

Bain & Company also warned of continued risks despite the potential “soft landing.” Many threats to economic growth have not been addressed, and, in fact, are unlikely to be solved in the short-term. Geopolitical conflicts, such as Chinese aggression in Taiwan or Russia’s invasion of Ukraine, could still interfere with a recovering economy.

Why There’s No Consensus

Economics is often condensed into the idea of the economic cycles. There are upturns, a peak, a crash, and then another upturn.

But predicting downturns isn’t that simple.

As we see in today’s economy, there are several variables that could tip the U.S. into recovery or recession. Many are outside of the Federal Reserve’s immediate control. Global conflicts, supply chain disruptions, and labor market shifts could all turn what looks like a soft landing into a definite downturn.

Unfortunately, we’re unlikely to know if we are in a recession for sure until after it’s occurred.

What Does this Uncertainty Mean for You?

The strategies used in an upturn are different from a recession. In a growing market, it’s possible to take more risks, while downturns require a greater level of conservatism.

It’s important to have a down-turn plan, no matter what your financial goals are. Having a strategy (and an emergency fund) in place makes it easier to make financial decisions with a clear mind.

After all, while we can’t predict the future, we can plan for it.

How to Juggle Growth and Wealth Preservation in an Uncertain Market

Without a clear consensus on the state of the economy, it can seem difficult to draft a financial strategy. Most advice on personal finance hinges on market sentiment. Therefore, living in a liminal, “in-between” state easily paralyzes individuals looking for a clear-cut answer.

But that doesn’t mean there’s nothing you can do to strengthen your financial position.

There are many additional tips outside of building your emergency fund, revising your budget, and diversifying your investments. Best practices for balancing growth and wealth preservation include:

- Using debt wisely. Paying off or reducing debt is important regardless of the market sentiment. However, blindly eliminating your debt can have consequences. Many discover that your credit score decreases when you pay off loans, which can make it more difficult to obtain decent credit for a home, car, or another big purchase. While you want to keep debt to a minimum, consider the kind of debt you hold, how easy it is to pay off, and your long-term goals before wiping the slate clean.

- Rethink major purchases. The total cost of a home or new car is definition not by the price tag but by the interest you’ll be paying on a long-term loan or mortgage. High-interest rates and an inflated market, combined with market uncertainty, can be a good reason to review your major purchase decisions and determine whether now is the right time to make them.

- Develop your creditworthiness. You may need access to credit down the road—make sure your score stays as high as possible through cash flow management. Small steps, like automating card payments or keeping your credit utilizaiton below 30% can help you better manage your current credit.

- Consider liquid and short-term investments. In the worst-case scenario, you may need more than what’s in your emergency fund. Shifting funds into short-term fixed-asset options with high-interest rates or in more liquid assets makes it more likely you will have access to cash reserved when you need it.

- Use multiple accounts. High-interest stress bank liquidity, thus increasing the risk of bank failures. You can potentially reduce risk by storing portions of your savings or investments at different banks, or by using brokerage-led cash management accounts (CMA). Unlike banks, brokerage CMAs do not lend your money. Instead, they generate revenue through transaction costs from their brokerage operations. As a result, these accounts generally do not have the same risks as banks. Many, in addition, are FDIC-insured.

You can also potentially improve your market position by working with trusted financial advisors, working with a tax professional to optimize deductions, and not making knee-jerk decisions to market changes.

But the number one thing to consider in an uncertain economic climate is mindset.

It’s important to note that not every strategy will be applicable to every portfolio. Differing goals, risk tolerances, and values all contribute to how you build and protect your portfolio. For this reason, it’s essential to slowly review all of your wealth preservation options with your long-term objectives in mind. Even good advice can give you anxiety if it doesn’t align with your underlying beliefs, anxieties, and hopes.

Often, the best thing you can do for your financial future is to take the time to fully understand your portfolio strategies and how they affect your wellbeing.

Want a second opinion?

Want some feedback

on your retirement plan? We can help.

With over 40+ years of experience in the financial sector, and as a licensed fiduciary, founder Jon Green can help you look over your retirement plan and understand whether you are on track.

You can book a complimentary session

or call me at +1 (828) 884-8840.