In November of 2021, the Federal Reserve had originally announced that they would gradually reduce their bond-buying over the course of 2022, thus keeping bank interest rates low. Only a month later, the government revealed they were shifting to a new strategy that they would finish this process by March 2022.

This means that higher interest rates are on the near horizon.

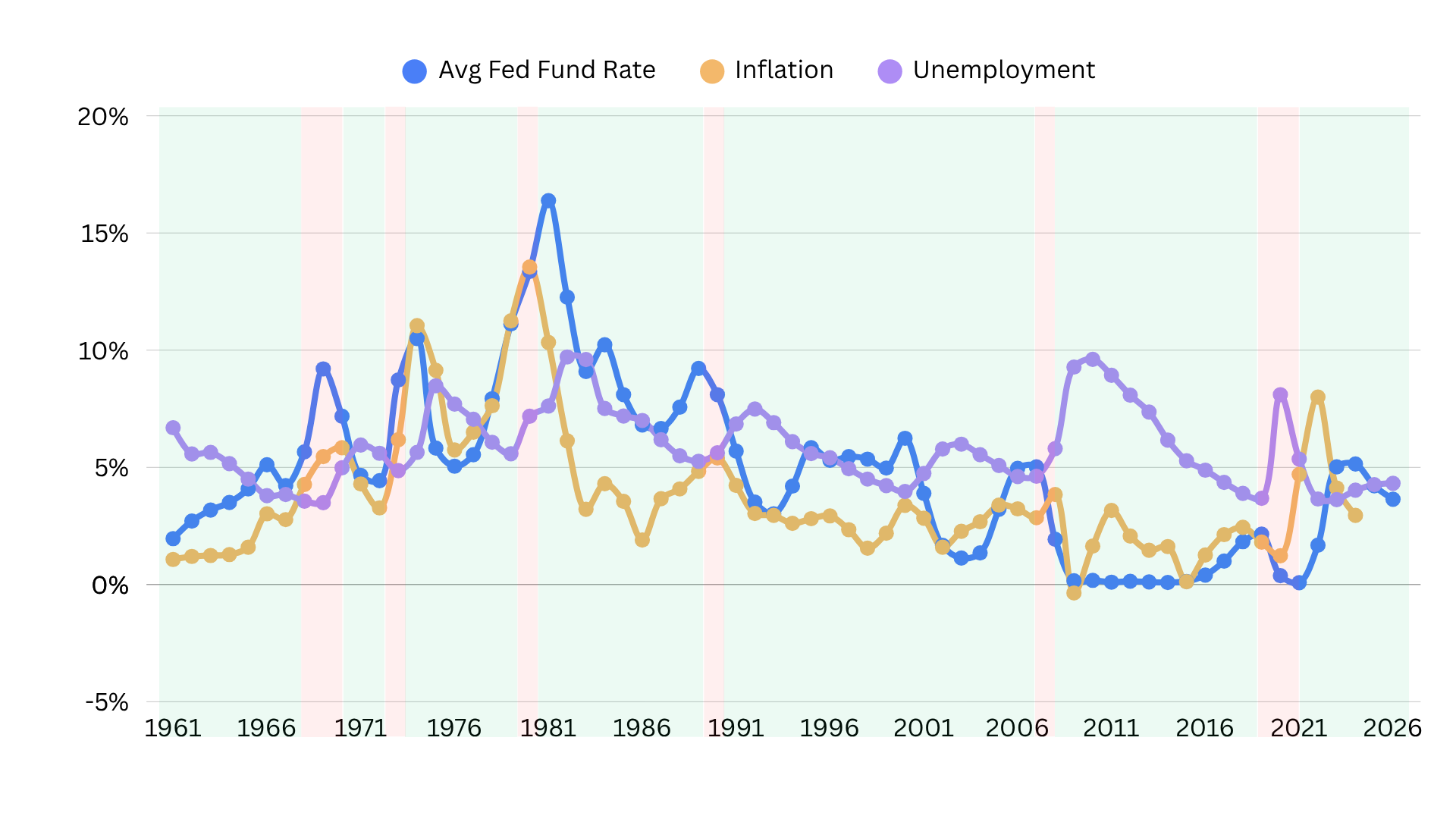

The Federal Reserve's goal is to reduce the inflation rate, which is at the highest it's been in over 40 years.

But for most savers and investors, the higher interest rate is an enigma. Questions run the gambit, but some frequent ones include:

- What does it really mean for retirement portfolios and savings goals?

- What interest rates are affected?

- Why will my bond value drop?

- Am I losing money?

It's true that every portfolio is unique, however, understanding how these rates work can help you decode your investments and plan accordingly.

Before we get into bond prices, we need to talk about what this interest rate is, and how it affects the market.

Direct and indirect effects of an interest rate hike

Contrary to popular belief, there is no "Federal Interest Rate". When the Federal Reserve raises interest rates, it is raising the Federal Funds Rate. This is the rate banks use to lend each other money overnight.

Why do banks borrow and lend to each other?

Every bank, including the Federal Reserve Bank, is required by law to have a percentage of its assets in liquid cash. As a result, banks will count their money at the end of every workday, and borrow funds from other banks if they come up short.

This rate directly impacts the prime rate, the secured overnight financing rate (SOFR), and bond interest rates.

However, credit interest rates and mortgage rates are also affected.

Why?

Because the banks and their competitors need to make money. Since they must now borrow and lend at a higher rate, they pass these costs to the consumer.

After all, if they are required to charge 3% between banks, why can't they charge the consumer 5%?

Alternative lenders, seeing that the banks are now charging 5%, may charge 8 or 10%. They can go higher since their competition has increased their interest rates.

As a result, there is a domino effect in the market.

The cost of goods, should, theoretically correct themselves. Or inflation should begin to drop.

But the cost of credit will go up, making it harder for individuals and businesses to obtain credit.

In turn, this will affect other aspects of the market, such as stock prices. Public companies often have some (or a lot of) debt. You can find out how much a company exactly owes in their prospectus, under the Debt-to-Equity ratio. When credit becomes more expensive, fewer companies will get the funding they need to grow or even stay afloat. Thus, higher interest rates can also cause fluctuations in the stock market that can affect an investor's portfolio, including their 401(k) and IRA.

So, just to summarize:

- The Federal Reserve will raise the Federal Funds Rate.

- This means banks have a higher interest rate to lend each other money.

- Fixed-income assets, like bonds, will be directly affected.

- Banks and their competitors (alternative lenders) will increase the cost of credit.

- This will likely increase interest rates for mortgages and other forms of credit.

- The stock market will be indirectly affected since it will be harder for businesses to get funding.

Will higher interest rates really stop inflation?

Hiking up interest rates is much like yanking the emergency break over and over. As consumer spending and bank lending decreases, the economy sputters painfully.

But it's better than perhaps driving off a cliff as inflation ramps up.

In context, it may be time for a market correction.

Consider this: the Federal Funds Rate has been abysmally low for over a decade.

In the unraveling of the 2008 economic collapse, rates dropped in September 2008 from 1.84% to .97% in October. In November 2015, it was at .15, just seven points higher than in 1954. In 2019, it was able to surpass 2% but then dropped again in 2020.

In terms of monetary policy, keeping the interest rate low inspires consumer spending and lending. But it also reduces how much consumers can get from their savings account. That .25% you're making on a "high-yield" savings account? That's because the interest rate has been low.

A higher interest rate, in contrast, makes money more expensive. It will ideally reduce spending, thus contributing to a drop in prices. That's the expectation.

Will it work? There are so many variables, it's impossible to give a 100% definite answer. But it's highly likely that it will.

For the financially savvy, this shift means it's time to reaccess your strategy - inflation or not. Here's why.

The link between bond prices and interest rates

One of the biggest changes in an interest rate hike is the drop in bond prices. In general:

- When interest rates go up, fixed-income prices drop

- When interest rates drop, fixed-income prices rise

This is especially true for bond prices.

When this happens, the most common question I get is:

"If my bond value drops, who will want to buy it?"

That's the wrong question. Current bonds basically go on sale. Think of secondhand clothing stores. You may get a $100 suit for $50 dollars. But it's lightly used and in good condition. It's a steal.

Consider this example:

- This month, you buy a bond for $100,000. This bond has an interest rate, or yield, of 5%, so you make $5,000 annually in cash.For those who are more math-minded, here is how the equation:$5,000 (earned interest) / $100,000 (principle) is .05, which is 5% (yield).

- In two months, bond interest rates are now 10%. And you decide to sell your $100,000 bond.

- But no one will buy it, because they can buy a bond that gives them a 10% yield. Your bond now needs to compete with bonds paying 10%.

- If you want to sell, you'll need to lower the price from $100,000 so that your return is a 10% yield. To make the interest rate work at 10%, you'd need to drop it to $50,000.

- For the buyer, they get a steal, since they are paying less than the regular $100,000 for a 10% return.

The key to not losing money is to keep the bond until it matures.

If you sell your bond, you lose $50,000. If you keep your bond, you will still get $5,000 a year.

In other words, if you chose to keep your bond, you would have made an additional $150,000 in 30 years. And you'd get you're original $100,000 back.

The main question is - do you trust your bond issuer?

If you've bought a bond from the US Treasury, it's probably fine. The risk is minimal for a government bond, as the US has a history of paying back its debt. But corporate bonds and other volatile fixed-income assets? That's another story. Will that issuer be able to pay you back over the years? Or is there a chance they might disappear?

The next question would be, do you need to sell early? If so, you may want to cut your losses, even if that means you'll lose money in the short term.

At the center of your decision should be logic and peace of mind. Just because the interest rate is going up and your fixed-income asset's value is dropping, does not necessarily mean your portfolio is in the red.

Your portfolio in 2022 and beyond

If rising inflation has been the primary focus of 2022, interest rates will be the highlight of 2022. Whether or not this shift in monetary policy fulfills its inflation expectation and lowers costs is yet to be seen.

But one this is certain - the financial market will be changing. And this process will continue for at least two to five years.

As a result, investors and financially-focused individuals should review their portfolios and reaccess their risk tolerance. Should you cut your losses on risky bonds? Will you want to buy a bond fund "at discount"? Individual stocks, mutual funds, indices, and other assets should also be reevaluated based on the new market risks.

Regardless, it can help to have a second opinion. Get in touch with our fiduciary advisors today to learn more.