Rising political tensions are affecting the financial markets in more ways than one. I feel the need to address the elephant in the room to properly prepare client portfolios. But I don’t want to speculate or fearmonger. Because the truth is that none of us are privy to close door conversations and back room dealings, whether that be from governments, corporations, or gangsters.

There are three political major pressure points straining our economy. When reviewing the following events, I’m not attempting to predict the future. These are neutral insights of incredibly (and sometimes horrifying) events that remind us of the importance of fiscal safeguards like emergency funds, cash management accounts, and flexible financial plans.

Below, I’m going to cover a few key factors that decrease trust in the dollar and why. These include:

- credit downgrades, the national deficit, and interest rates,

- antagonist towards the Federal Reserve, and

- geopolitical escalations, especially given recent events in Greenland and Venezuela.

This breakdown is not a forecast or speculation. Nor is it advice or a recommendation. It is not an indictment of political preference.

Rather, I aim to explain how these policies are destabilizing the economy and creating confusion for investors at home and abroad—all of which affects your portfolio’s value.

Downgrades, deficits, and interest rates

Each government deals with the deficit differently. However, the current trajectory and abrupt policy changes have been central to discussions around President Trump’s economy since the beginning of his second term.

Looking back at May, 2025, there were already concerns around the federal deficit. That month, Moody’s downgraded the United States’ credit rating. Why? Congress appeared likely to add trillions to the federal deficit through the One Big Beautiful Bill Act. This legislation eventually passed, and is on track to add $3.4 trillion to our debt over the next 10 years.

The debt alone creates a significant hurdle. While we have never defaulted, the combination of a rising deficit with lower trust strains federal funds.

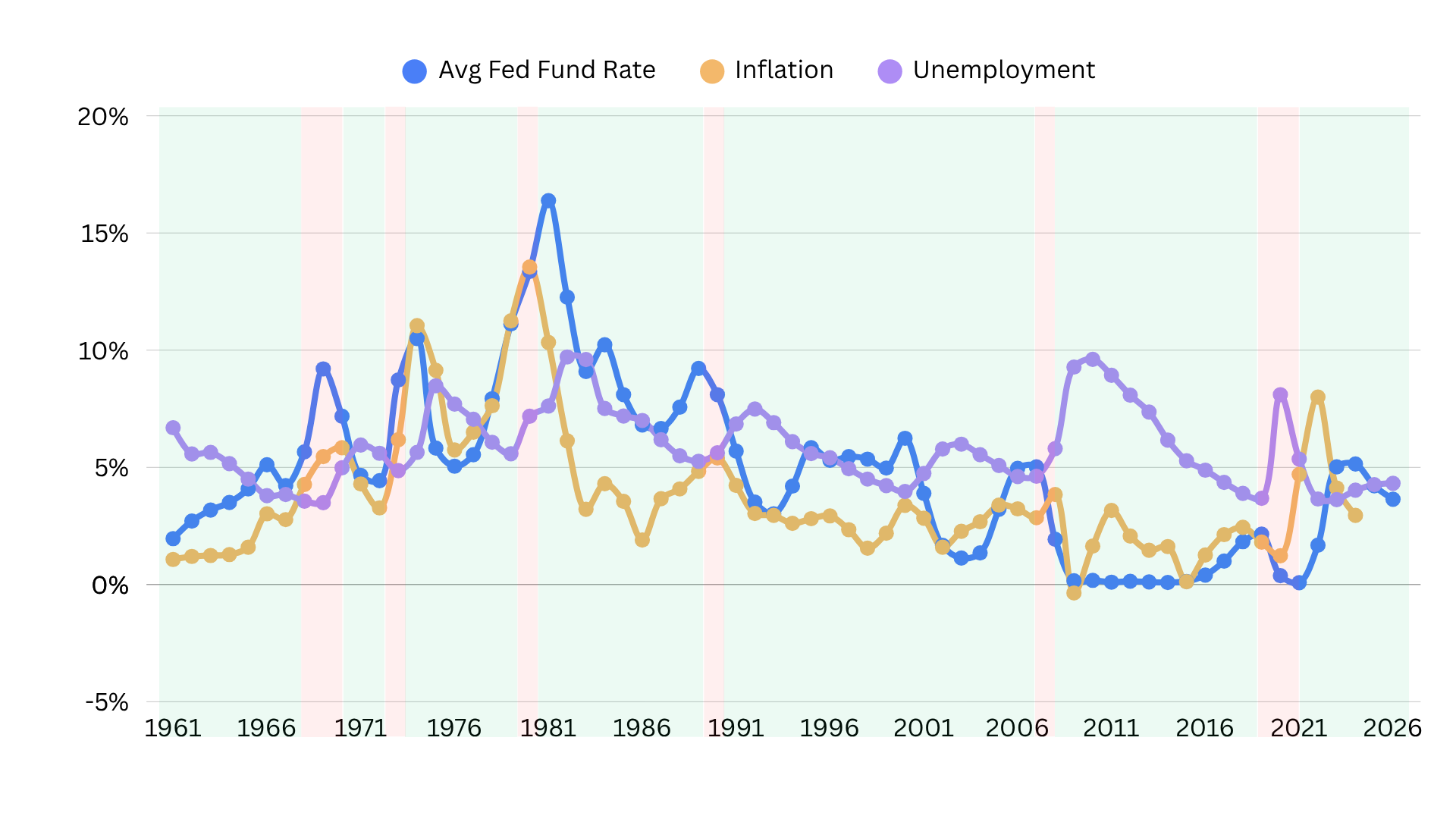

Let’s also mention interest rates and inflation. President Trump has advocated for rapid rate cuts, and even suggested a 10% interest cap on credit cards. His rationale is that lower interest rates will boost affordability, lower inflation, and improve spending.

Unfortunately, the math is more complex.

Reducing interest rates can make credit more affordable. However, lower rates do not mean lower inflation. After all, the inverse is often true. Central banks often raise interest rates to limit inflationary pressures, and lower them when the dangers are long past.

It’s true that inflation has been in decline. Yet, this does not translate into rapid rate cuts.

Let’s look at Turkey for a modern example. Turkish President Erdogan believed that high interest rates caused inflation, and he pressed the central bank to dramatically decrease rates. His approach was so aggressive and so quick, that inflation skyrocketed to 85%. The American Enterprise Institute has an excellent summary of this crisis and how it was resolved (in short: Turkey raised interest rates to 50% within the year).

Turkey isn’t the only example. I’ve written in the past on how authoritarian approaches to economics simply don’t pan out in the long-term.

Economics relies heavily on math and statistics, but with a complex economy there are hundreds of variables involved. We need trust in fiscal institutions staffed with experts to make sound decisions around monetary policy, regardless of who is in office.

Unprecedented: Suing the Federal Reserve

One of the most bizarre events in my lifetime, and I am confident many financial advisors will feel the same, is the current antagonism towards the Federal Reserve.

Whether you believe in big government or small government, whether you’re a republican or democrat, that’s not what this is about. The Federal Reserve can develop and enforce good policies as well as bad. This department and the federal government should work in unison to protect US economic interests.

Yet, we have the federal government suing the Federal Reserve after a barrage of personal attacks against the Chairman Jerome Powell. That kind of friction sows distrust in our institutions. And I’m the first person to tell someone what I honestly think, but this is a significant problem because it politicizes the Federal Reserve.

Traditionally, the Federal Reserve has enjoyed a certain degree of autonomy. Since its founding in 1913, the Fed has been able to operate without significant bureaucratic hurdles. When other countries still had politicians and monarchs entrenched in the Treasury, we separated State and Funding.

Monetary policy decisions did not need to be approved by the president or by anyone else in the executive or legislative branches of government. That’s lean governance.

This is the first time in history that the United States government sues the Federal Reserve. Now, this isn’t to say that the Federal Reserve has never been sued. It has. We’ve just never had the government take part.

Why is President Trump threatening a lawsuit?

He claims it relates to a renovation misquote. However, President Trump has also repeatedly demeaned Chairman Powell for not lowering interest rates fast enough. And this behavior poses the problem, not about economics but about department autonomy and trust. This is not a question about right or wrong, but about how we handle working relationships successfully.

This hardliner approach, in the finance world, simply does not work.

Conflict shakes investor trust — both domestic and international. If global investors become adverse to the US economy, this sparks bad news for reducing our ballooning deficit.

A day after the announcement, the stock market opened lower, the dollar’s value decreased, and financial experts speculated if U.S. bonds would face another sell-off.

If investors begin selling off U.S. bonds in bulk, we will run out of money for the government to function. The deficit will crush the economy.

The Cost of Greenland, Venezuela, and Other Geopolitical Tensions

We’ve seen increased geopolitical tension across the globe, regardless of who is sitting in the White House. Russian aggression in Ukraine began in 2014, for example. Tension between China and Taiwan extends back into the 1950s. Israel and Palestine have been at odds since 1948, and Iran has suffered instability for decades. The current Sudanese Civil War began in 2023, but we’ve seen conflict coverage since the 1980s.

But when we turn on the news, it often feels like these situations have gotten worse.

The current administration takes a different approach from its predecessors, both Republican and Democrat. Butting heads over allied nations to acquire Greenland, for example, has created confusion.

Our NATO allies are beginning to pull away from the United States, fostering distrust between our long-time partners in Europe. Regardless of whether or not we should acquire Greenland, the current approach strains investor relations.

And it’s not just international investors we need to worry about. Greenland will have a price tag. Bought or conquered, it costs money. One range estimates this island would cost the American taxpayer $500 to $700 billion dollars. Ouch.

Our recent foray into Venezuela isn’t fairing much better. After violating international law to kidnap the Venezuelan head of state, President Trump states that the oil industry would invest $100 billion. But oil executives claim that the poor state of oil infrastructure and oil quality makes Venezuela “uninvestable.”

The question with Venezuela remains: If the oil industry won’t invest, will the taxpayers be subsidizing it?

These are just two ongoing geopolitical conflicts that could add to our deficit. When handled poorly, these conflicts could erode trust in United States leadership and profitability, leading to downward spiral.

The key phrase here: could.

We cannot speculate on how our leaders in the government and private sectors will act. There is always a probability of success, even slim. However, the tides are tumultuous, and wealth management focuses on risks.

The risk of increasing the deficit and further reducing trust in America is high, at least in the short-term. All of this weakens the dollar, our economy, and our spending power. When this happens, our retirement dollars don’t stretch as far, our quality of life declines, and our children worry for their future.

It doesn’t have to be that way. But, for now, the uncertainty means we likely should take a more cautious approach to our finances.

My professional perspective: Let’s talk about it

With this degree of volatility, I’m not willing to stake even a two-year forecast of events. It’s a new era, changes are rapid, and attempting to pin down where we will be in one, five, or ten years feels unprofessional.

However, my aim is to help navigate my clients through the financial world, in good times and bad. Luckily, I have decades of experience under my belt. Our economic uncertainties are new and the system has changed. But I’ve weathered more than one storm, and as an objective advisor, I’m legally obligated to give clients the best advice possible for their specific portfolio.

Outside of the general best practice of keeping an emergency fund, I can’t give advice unless I speak with you and see your portfolio. Like with economics, there are variables. Your current financial health, your goals, your lifestyle, your values—these all matter when it comes to financial planning. There is no “one-size-fits-all” approach.

I’m free to discuss your thoughts and answer your questions at any time. Book a complimentary introduction session today to get started. Or subscribe to my newsletter to get more economy and financial planning insights.