Running out of money in retirement is a significant problem. But the good news is that there are things you can do to make your hard-earned dollars last longer.

Before we go over our 8 factors to maintain your savings, we first need to dive deep into why people run out of money in the first place.

Why do people run out of money?

There are several reasons why people run out of money in retirement. This includes wealthy individuals or those who had high incomes. And the reasons are far simpler, in most cases, than you might think:

- Failing to set a date of when you will die - Death is an emotional topic, and most of us prefer to avoid thinking about it. But if you want to successfully plan for retirement, you need to understand how long you might live post-retirement in order to calculate how much you need to save.

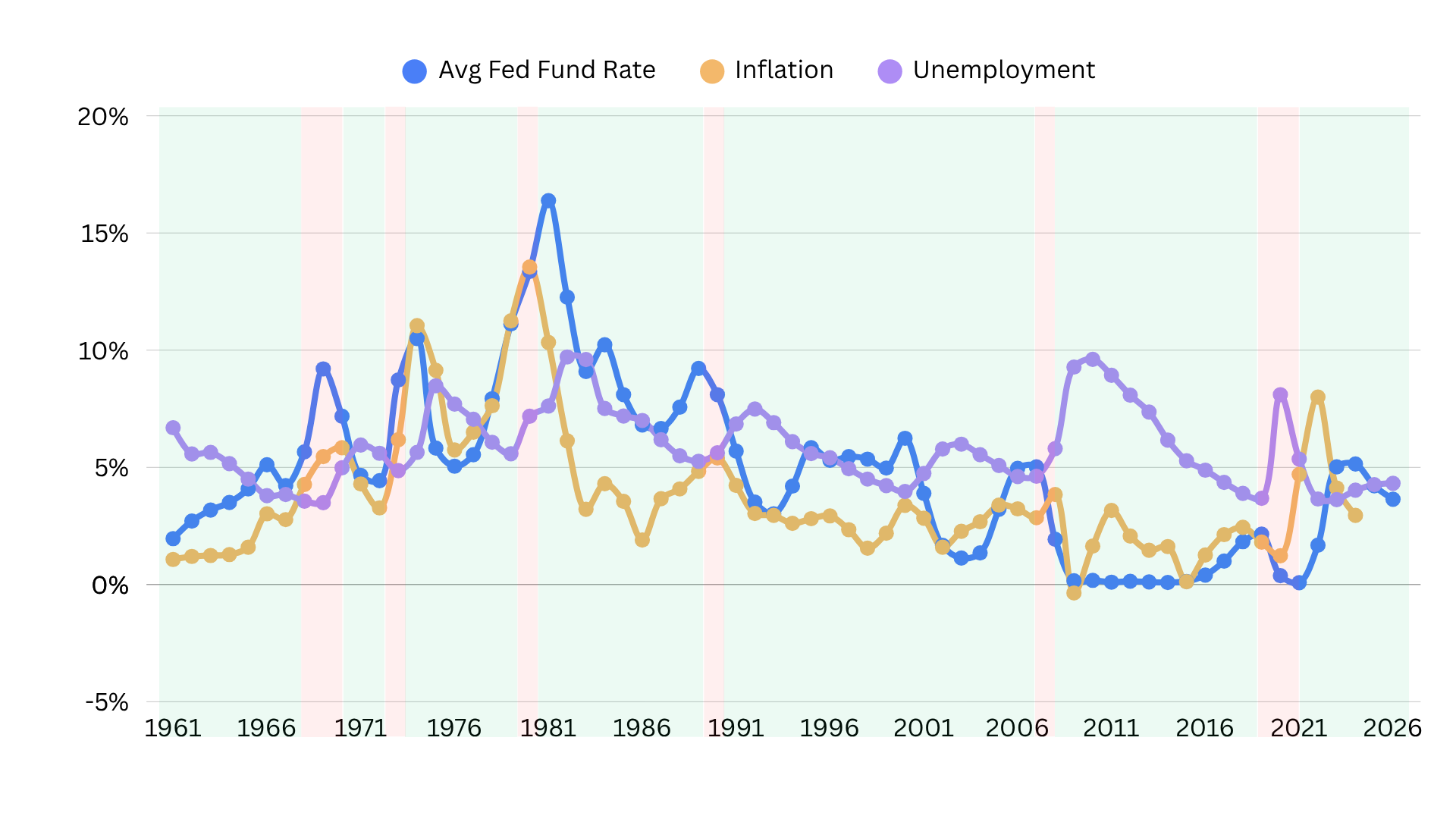

- Misunderstanding the present and future value of money - There’s a big difference between the value of money today and the value of it tomorrow. Due to inflation, $5 could be worth significantly less tomorrow. But if you’ve added that $5 to an investment that reinvests dividends, you could at least be keeping up with inflation.

- Being too inflexible - There are many variables that affect where you are going to run out of money. This includes returns. You can’t assume that your returns will remain the same every year, or that they will be a certain percentage point. It’s good to plan for the worst-case scenario and adapt your retirement plan as you grow.

- Underestimating the cost of mental health in retirement - We all pretty much assume that we’ll need to fork over a lot of extra cash due to healthcare expenses. Higher premiums and hip replacements aren’t cheap. But mental health costs may also skyrocket, and they may not be covered under your insurance plan.

- Not adapting with their plan over time - One of the biggest things people forget is that your assets and needs change as you grow older and the economy changes. You’ll want to adjust your plan here and there as your appetite for risk or requirements changes.

- Not using the right tools - An excel sheet is OK, but you really need mathematical models in order to actually project your retirement savings with a degree of accuracy. These tools are rarely available to individual investors. So it can help to have a dependable advisor to help you review your retirement plan.

The 7 most important factors for a successful retirement plan

Finally, there are at least 7 concepts you need to be aware of if you want to reduce your chance of running out of money. Some of these are relatively obvious. But others are far more complicated.

In order of importance over your retirement portfolio, here are 7 concepts you need to master:

1. Adjust your spending

This might seem like an obvious one, but you really need to understand how much you are spending today and how much you will need in retirement. Even if you have saved $5 million, if you burn through $100,000 a year, it won’t last long.

2. How much money you have

How much money have you saved? You can save more if you spend less today. This doesn’t mean you need to be a miser, but it can help you save if you know the value of what you’re buying today. It’s also recommended that you put your savings into various investments in order to gain dividends and grow your wealth.

3. Where you take the money from

Most people have a joint account where money is taxed when it goes in. They also are likely to have an IRA and 401(k). But what are the tax implications? Understanding how you take money out is crucial, as you want to reduce your taxable income and avoid penalties.

4. Choose how long to plan for

How long do you plan to be retired? Do you plan to retire at 40? 50? 70? And how long will you likely live after retirement? Understanding this variable is simple enough, even if you can’t pin down the exact year. It’s better to be conservative and plan for a longer retirement than a short one.

5. Planning for inflation

When calculating your required savings, you need to take inflation into account. Every year, the value of the dollar drops between 1-3%. Your savings should keep up with inflation, if not surpass the rate. If your investments are providing a return, after fees, of 3%, it’s probably too low and you may need to be more aggressive.

6. Estimate rate of return

While your rate of return will fluctuate based on a variety of factors out of your control, having a general estimate can help you understand how well your wealth is growing if it’s keeping up with inflation, and if you’ll be able to retire on time. It can also help you decide which assets to let alone in your earlier years, so you can let those accounts continue to grow.

7. Invest to generate interest

Generating interest and dividends is essential to creating a post-retirement income stream. You’ll want to make sure that your nest egg continues to work for you, even when you’ve decided to throw in the towel and relax on a beach.

Want a second opinion?

Want some feedback

on your retirement plan? We can help.

With over 40+ years of experience in the financial sector, and as a licensed fiduciary, founder Jon Green can help you look over your retirement plan and understand whether you are on track.

You can book a complimentary session

or call me at +1 (828) 884-8840.