Whether you live in North Carolina or are fascinated by The Old North State, there comes a time to think about the best place to retire. And for many, North Carolina is the perfect place to spend their golden years. When you already have a home, family, and friends, why would you move? But it’s not that simple for other retirees.

For example, after 50 years of living in Raleigh, you may want to move to the rolling hills of Transylvania or Madison county. Or, maybe you are a through-and-through Tennessean, but your only child is working in Charlotte—and that feels close enough to be home.

Regardless of the reason for retiring someplace new almost always comes down to one thing: Not running out of money. In this article, I’m going to break down key money considerations for retirees specific to North Carolina.

6 Considerations for Retirement in North Carolina

The highest costs you’ll face are housing, healthcare, and taxes, no matter where you live. Yes, some states are more tax-friendly than others, but it’s important to maintain a balance of low-taxes and quality of life. That’s why, when talking about living in North Carolina as a retiree, I’ve also included cost-of-living estimates, lifestyle expenses, and climate concerns.

These factors are ordered from most-to-least important, but these items should be a part of every retirement plan:

Healthcare

When it comes to healthcare, North Carolina is average compared to other states, holding the 25th spot in the US News rankings. But not every county is made equal. According to County Health Rankings, Wake County (known for Raleigh) and Orange county have the healthiest populations and the highest life expectancies. Residents live to 80 and up.

At the same time, North Carolina is subject to the same healthcare challenges as the rest of the country. Hospitals, especially in rural counties, are bought by private equity, driving costs up and lowering healthcare quality. We’ve seen it in Transylvania county—but it’s a nationwide problem. It’s important to investigate your potential healthcare costs and options in your ideal area ahead of time.

Housing

If you already live in North Carolina, housing may be less of an issue. However, you may be interested in downsizing or moving to reduce property taxes or be closer to family. For people looking to move from other locales, affordable housing is critical—especially if home values in your current state are lower than in North Carolina.

There are a wide range of options when it comes to affordable housing, from $114,000 in Roanoke Rapids to the median $600,000 in Transylvania County. But buying a house and reducing taxes isn’t everything. Home maintenance and home insurance can dramatically increase costs. You may want to investigate other options, such as senior living options or housing communities to offset these expenses.

Cost of Living

When it comes to overall living costs, North Carolina sits in a healthy median. There are many variables to consider, despite expert estimates. For example, an article in the Charlotte Observer stated that you could live for 17.5 years off of $1 million dollars. But that very well may be shorter or longer depending on your lifestyle, county, and health, among other factors.

Looking at a report from Unbiased America, there are some NC rates compared to the national average:

Electricity, water, gas/fuel, internet, and cable cost 6% less than the national average

Groceries cost 12% less

Gas and oil are 27% less

Healthcare is 12% above the national average

Of course, this changes depending on your location, whether that be county-to-county or state-to-state. For example, the cost of living is 16.5% higher in Los Angeles, CA than Charlotte, NC. Meanwhile, residents of Jackson, Mississippi will find Charlotte to be 24.6% more expensive.

Weather and climate

Weather patterns matter, especially as you age. There’s a reason many people choose to retire in Florida, after all—and they are more likely thinking about the beach than taxes. But, in all honesty, weather and climate patterns affect more than just your mood.

Your environment also affects your home insurance costs, emergency preparations, and health. North Carolina features a temperate climate and four seasons, but Hurricane Helena created a new awareness of a changing climate. Being aware of these risks will help you avoid potential additional costs and choose a safer locale.

Lifestyle

Hobbies in retirement matter. The last thing you want to do is sit around doing nothing, just to make your dollar stretch a little further.

That’s why it’s also important to consider what your perfect retirement state can offer. North Carolina offers a little something for everyone. Residents can enjoy various outdoor activities with access to both beaches and mountains. Cities like Ashville, Raleigh, and Charlotte all host a number of art galleries, restaurants, gardens, and other leisure options.

This variation is ideal for the retiree. While you likely have an idea of a hobby or two you’d like to pursue, you may discover new passions as you grow your community.

Taxes

It’s common for retirement advisors (and your average online article) to begin with tax benefits of your retirement state. It’s true that taxes affect the longevity of your retirement income. But, when compared to the other financial considerations, it is hardly the most important factor.

After all, if you own your home, live close to family, engage in hobbies, and can afford the cost of living—taxes may be minimal. For someone moving from a state with lower taxes, such as Florida or Tennessee, the tax code matters more.

Overall, the Tax Foundation ranked North Carolina as the 13th state for tax-friendliness. It leverages a flat 4.25 percent individual income tax rate, as well as county-specific property taxes. For example, the annual property tax of a $500,000 home in Transylvania County is $2,375, or a 0.475% tax rate. Sales tax also differs, with rates ranging from 4.5% to 7% depending on the county.

All of these rates should be included in your retirement calculations.

Retiring in NC:The Cost of Raleigh

*Disclaimer: Below is a hypothetical story based on a generic client profile and should not be taken for financial advice. It is an illustrative example of how people can analyze their money to make big life decisions.

Let’s say that Sarah Cohen of Duluth, Minnesota wants to move to Raleigh, NC. She loves the climate and the outdoors. Her favorite cousins and their children live in Greensboro, just an hour away. There’s a thriving Jewish community, and an endless list of activities for the area. Of her three children, one is in Asheville, another in Chattanooga, and one lives in Minneapolis—so she would be closer to two of her three kids. But Sarah would still have space for herself.

Sarah’s question: How much does she need to live in Raleigh—and will her portfolio of $2 million cover it?

Let’s start with housing.

After selling her home for $326,617, Sarah will have enough to cover most of a mortgage. After home improvements, closing fees, moving costs, and other fees, she’ll have $280,000 to put towards a house.The median home cost in Raleigh (at the time of writing), is $427,483. If she spent the profits from selling her house on the downpayment and closing cost, her mortgage would only be $991 a month.

Next, let’s look at taxes. North Carolina has an income tax of 4.50%, while her income tax in Minnesota was 7.85%. Even the lowest bracket in Duluth was higher than in NC, so she spots some savings there. The property tax also drops, from 1.34% to 0.750%.

What does this look like? Well, she’ll be paying $3,203 in property taxes instead of $4,069—$1,000 saved just from property taxes alone. Income, of course, will differ by how much she takes out of her account.

The cost of living is marginally higher in North Carolina, around 3.8% excluding housing. But most of the expenses revolve around eating out, car costs, shopping, and utilities. There are obvious ways to cut down these costs—such as eating at home more frequently, keeping her current 3-year old car, and adding green improvements to her new home to lower costs.

Once she retires next year, she’ll get $3,087, or $37,044 per year from Social Security alone. Withdrawing 1% from her 2 million retirement assets per year would give her $20,000—enough to meet the minimum for meeting the same living standards in Duluth.

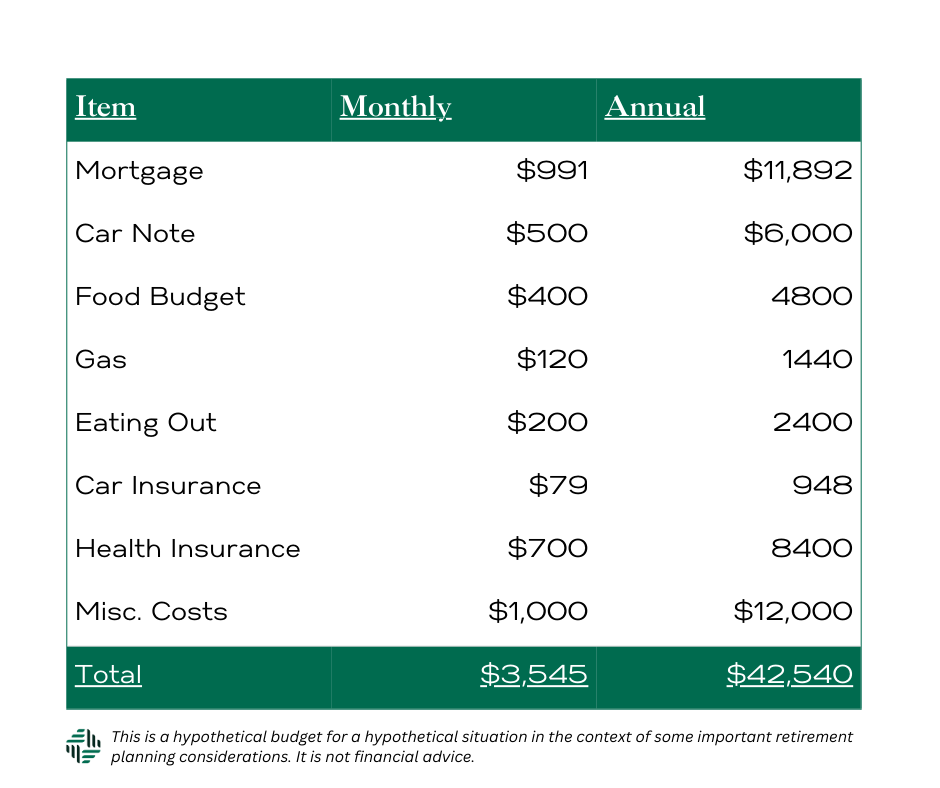

So, knowing these costs (and savings), she writes down a general list of expenses that she can predict:

With this list, Sarah estimates that the cost of utilities, home insurance, additional savings, and unexpected expenses all need to be added. She just isn’t sure of the cost yet. But, according to other estimates, there is $10,000 missing from her sheet. Ten thousand she can easily make up and can expect after the move. Knowing that this amount is easily covered, Sarah feels that moving to Raleigh is financially feasible.

Even if she only takes out $20,000, or 1% of her retirement assets every year to support her social security, she’ll only lose $160,000 over 8 years. If she can save a little extra or take out last, her month will go even further in the long-run.

Get Local Advice

In the above example, Sarah is working with a lot of generic information on North Carolina. But there’s a difference if you already live there. And it helps to have a local advisor who knows state-specific challenges and opportunities.

Encompass Advisors is a Registered Investment Advisory (RIA) firm nestled in Brevard, North Carolina. We provide objective financial advice to clients living down the street and around the country.

Want some feedback on your retirement plan? We can help.

With over 40+ years of experience in the financial sector, and as a licensed fiduciary, founder Jon Green can help you look over your retirement plan and understand whether you are on track.

What are we doing over at Encompass Advisors? When we aren’t speaking with clients, we are watching the markets and running numbers. Get our latest, in-depth insights here.