Will the housing market crash, or are we just seeing a slight slowdown?

That question has been on our minds for a while now. And while we are certain that there's a housing bubble, it's impossible to predict when the real estate market will officially see a slowdown in house price growth, let alone a market crash.

What we are looking at is a unique situation in the housing market. Unlike the Great Recession of 2008-2009, this housing boom isn't predicated on subprime loans. But we are dealing with significant inflation pressures, a shortage in the housing supply, astronomical price increases for purchasing and renting, as well as higher mortgage rates.

To get a better overview of the potential housing market bubble, we need to consider what has been driving the real estate market over the past few years and how these pressures and policies will affect more than house prices.

Decoding Housing Market Pressures

Like in any market, there are a lot of moving pieces. For example, there are plenty of reasons to believe that the housing market is healthy, even as the housing boom is clearly in decline. Some professionals like to cite that:

- There’s a lot of demand for housing for Millennials and Gen Z

- Supply can’t keep up with demand -we have a housing shortage

- Tighter credit regulations translate into fewer defaults

That said, many housing experts aren’t too sure that these claims are as solid as they look. Current pressures affecting the real estate market include:

- Despite the high demand, the spike in housing prices has locked many potential buyers out of the market

- Rising interest rates make moving and purchasing homes more challenging

- Continued inflation, bolstered by supply-chain issues, the Ukraine-Russian conflict, and similar regional issues, reduce consumer spend

- Investors bought 24% of single-family houses in 2021, thus putting pressure on the housing supply

- Rent has increased up to 40% in some areas, leading to fewer buyers pursuing home purchases and in some cases, increased homelessness

All three of these challenges link tend to cause real estate band housing bubbles. And according to Jeremy Grantham, co-founder of the GMO investment fund, we are likely to see housing bubbles not just in the United States but worldwide.

Both China and India have seen a slowdown in the housing market. That doesn't mean there is going to be a global financial crisis, necessarily, but that investors can expect long-term effects in the global real estate market.

The Federal Reserve’s Role in the Current Climate

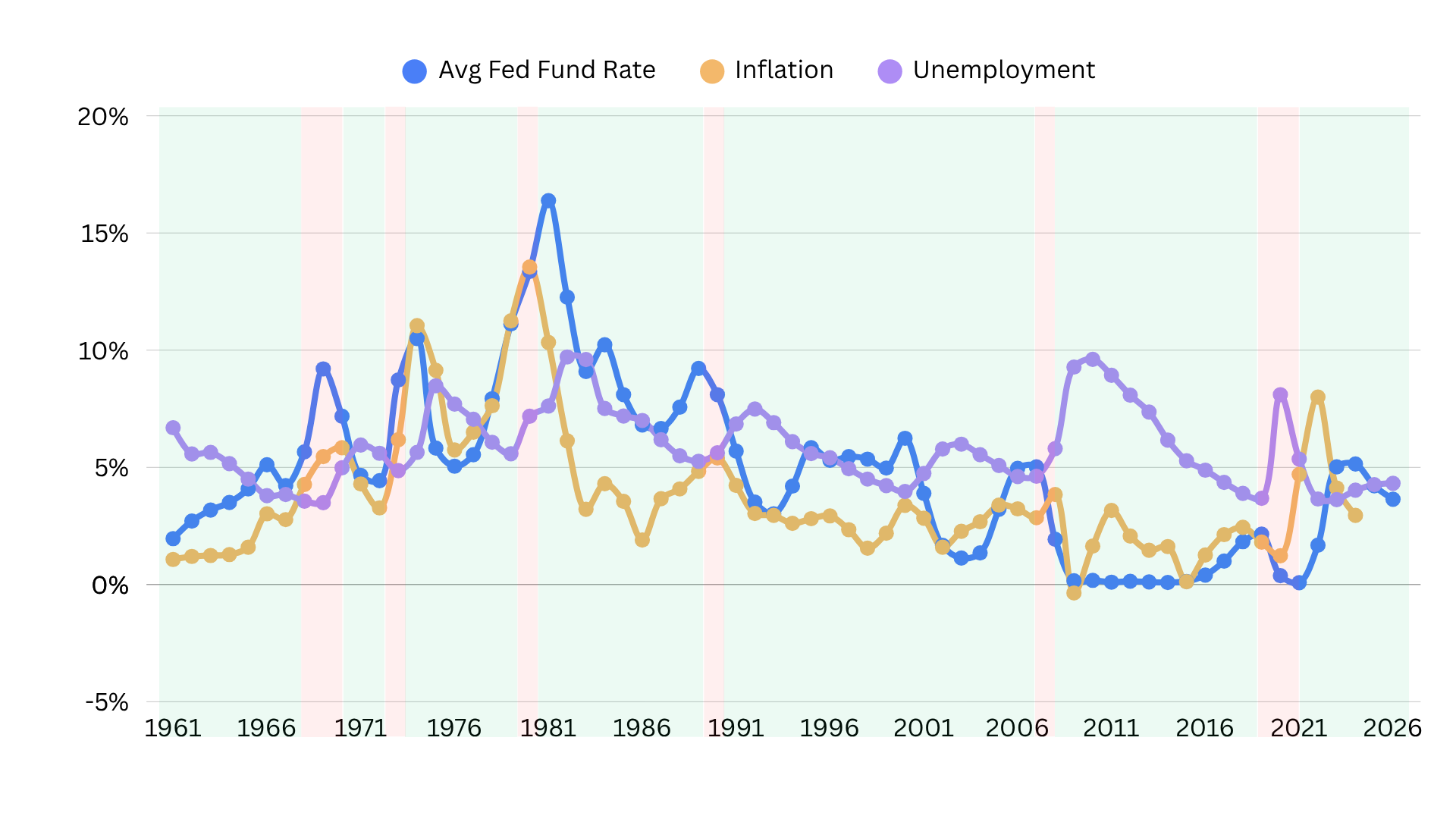

The Federal Reserve’s policy of dirt-cheap interest rates may be over, but it’s potentially caused significant distortion in the housing market.

Here’s what happened:

Interest rates have been low for well over a decade, but the economic trauma brought on by the pandemic caused the Federal Reserve to old tactics. Not only did it cut rates to zero, but it aggressively bought up several long-dated government bonds and mortgage-backed securities (MBS). As a result, the Federal Reserve now owns 40% of the MBS market.

This strategy ensured that mortgage rates would plummet-making home-buying more affordable. And the Fed kept buying up MBS as the housing market spiked.

But as the monetary policy weens off of quantitive easing, the Fed will likely be stuck with its current MBS portfolio for years. Even if housing prices decline, higher rates coupled with stagnant wages and a potential recession translate into fewer moves and relocations, thus fewer new mortgages.

What all of this means is that many Americans will be stuck with their current assets. And this is a problem in the sense that purchasing a home has always been a cornerstone of wealth building. A slower housing market can intensify pressures in an already slow economy.

So, what happens if there’s a bubble?

What Happens If the Housing Market Crashes?

To be frank, it depends. We can’t predict with any accuracy what will actually happen when the bubble bursts. But we can get an idea of potential scenarios.

First off, if the United States slides into a recession (and some analysts believe we’re already in one), then this may be a good thing for the bubble. While initially, the recession would further slow down the market, once it hits a certain low price level or mortgage rates, consumers will begin buying again.

This is an ideal scenario. If we consider the current employment gap, a recession could happen with minimal layoffs-at least compared to the 2008 crisis. If we can forgo mass unemployment, some of the effects of a recession could be reduced.

However, we also want to look at a worst-case scenario. Just to prepare ourselves and our portfolios.

If the bubble bursts, we’ll likely still have some lingering effects, such as:

- Layoffs and increased unemployment - Several industries could be affected here, including real estate, finance, and construction. While many job openings are available across the US and a labor shortage continues, professionals from these industries may need to shift into other sectors, some of which will be lower-paying.

- Homebuilding - With the increased demand for housing, there is an opportunity for developers. The problem is that when a housing bubble bursts, the demand will shrivel up. Again, this can lead to layoffs, unfinished projects, and supply chain issues for homebuilders.

- Shift in spending - Many consumers will go into “savings” mode and with high mortgage rates, may forgo homebuying as a form of investment. This is especially true as the cost of renting has increased exponentially since the pandemic.

Some experts believe the housing bubble is part of a larger superbubble, including over-valued equities and securities. If the entire thing goes bust, we look at significant devaluation across financial markets.

But even if we’re lucky and only experience a mild slowdown in economic growth, it helps us prepare. Most recessions last 2-5 years, with some lingering effects thereafter. Having an emergency fund and access to liquid cash, reducing riskier investments, and putting money in inflation-resistant commodities can offset potential drawbacks.

Of course, every portfolio is different. During times of uncertainty, make sure to speak to your trusted financial advisor to reevaluate your goals and review your portfolio.

Want a second opinion?

Want some feedback

on your retirement plan? We can help.

With over 40+ years of experience in the financial sector, and as a licensed fiduciary, founder Jon Green can help you look over your retirement plan and understand whether you are on track.

You can book a complimentary session

or call me at +1 (828) 884-8840.