Deciding when to start your social security benefits can be confusing, especially as you transition from work to retirement. Because there are so many moving pieces to your finances, it’s important to sit down and weigh the pros and cons of waiting until 70 or applying once you hit 62.

There are ways to simplify the process. Namely, it’s essential to estimate your life expectancy, decide when you plan to retire, review your current retirement portfolio, and define your retirement and inheritance goals. These variables, along with understanding how social security works, can help you decide when to take social security.

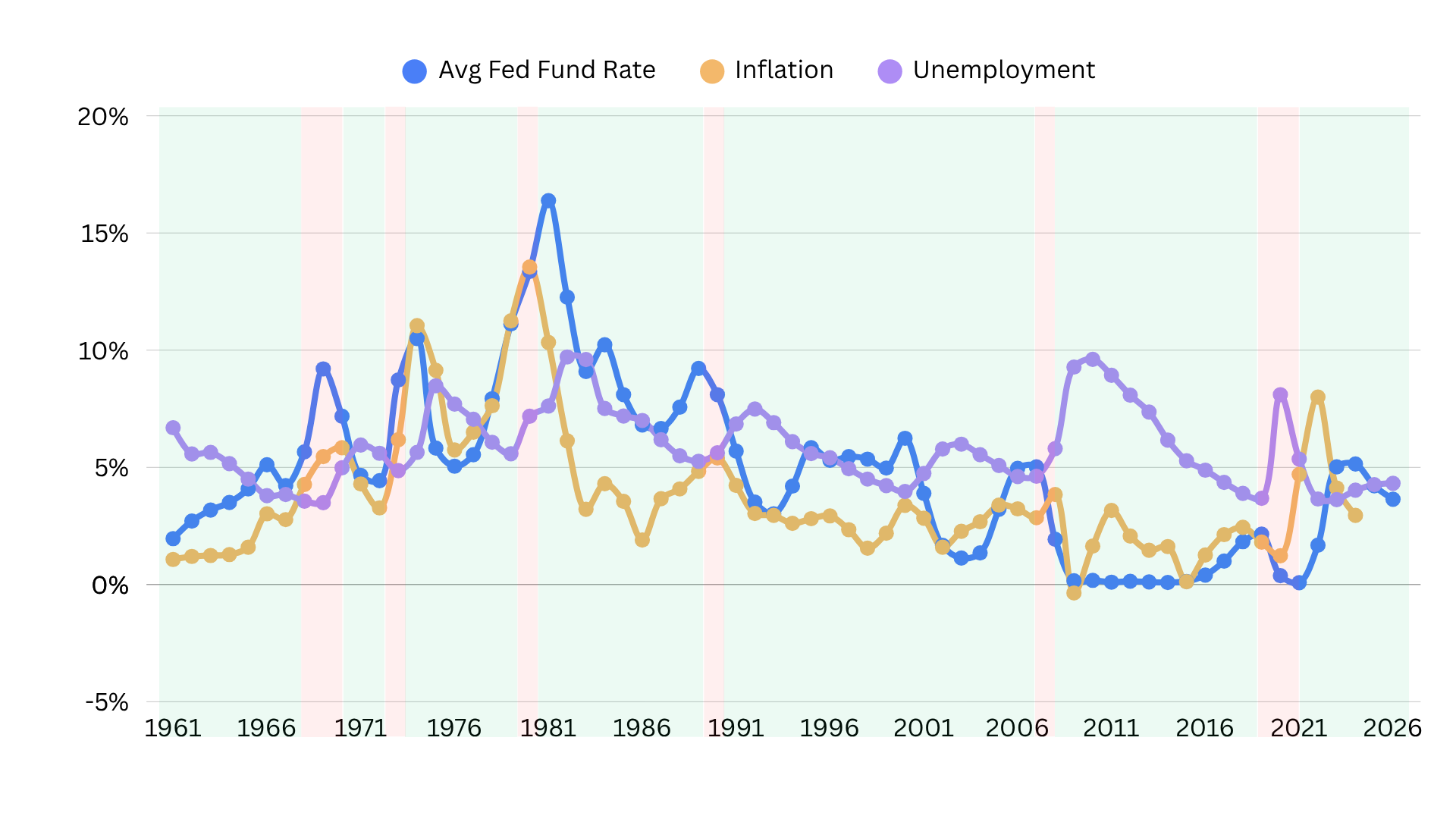

Social Security Basics

You can choose to start taking social security between ages 62 and 70. The amount you receive depends on two factors:

- Your average earnings

- The age of your claim

Your earnings doesn’t just mean your salary. It also relates to your bonuses, commissions, and vacation pay. The Social Security Administration doesn't count pensions, annuities, investment income, interest, veterans benefits, or other government benefits.

The calculation is rather simple:

If you are under full retirement age for the entire year you file a claim, the Social Security Administration deducts $1 from your benefit payments for every $2 you earn above the annual limit. When you reach full retirement age, this drops to $1 deducted for every $3 you earn above the limit.

The key here is “full retirement age.” As of writing, it is 66 and 10 months for people born in 1959 and 67 for those born in 1960 and later.

In other words, you can take social security at 62. But that’s not always the best option.

Why Wait?

Choosing to wait for social security stems from the approach that the longer you wait and the longer you contribute, the more you’ll get.

Let’s say you were born in 1950 and plan to receive benefits in 2026. Your estimated earnings are $46,000.00, meaning your estimated monthly benefits would be:

- $1480 if filing at 62

- $1973 if filing at 66

- $2604 if filing at 70

We can see that the difference is over $1,000! It’s clear that waiting even until 66 may benefit your retirement income. But that’s not the perfect situation for everyone.

Why Apply for Social Security Earlier?

There are many reasons you may choose to apply at retirement age rather than the “break-even” age. One of the most prominent concerns today is the idea of insolvency. Social security is considered solvent so long as its trust can pay 100% of currently scheduled benefits. In it’s 2025 Trustee Report, social security is set to be depleted by 2033. At that time, it will only be able to pay 77% of benefits.

For that reason, it’s tempting to start taking your funds immediately. The belief that this will lock you into your benefits.

There are other reasons, too. Disability, wanting more time for an active retirement, and simply not being dependent on social security all contribute to wanting to cash out earlier than 62 or 66.

Furthermore, if you are married and have a lower average earning than your spouse, you may choose to take your social security early while waiting on the larger income.

Get Objective Advice

Ultimately, I always give my clients a quick test to determine if they should take social security earlier or later. I ask them to consider how long their parents or grandparents lived. If family members tend to pass by 60 or 65, taking the money earlier might be a good idea. But if your parents were active into their 90s…waiting until 70 may be more beneficial.

Deciding when to take social security benefits is just one aspect in a long line of retirement planning tasks. It’s often challenging and complex to do it alone. Speaking with an objective financial professional helps.

As a fiduciary, I am legally obligated to give you objective advice. If interested in a second opinion, book a no-commitment call with me today.

Want a second opinion?

Want some feedback

on your retirement plan? We can help.

With over 40+ years of experience in the financial sector, and as a licensed fiduciary, founder Jon Green can help you look over your retirement plan and understand whether you are on track.

You can book a complimentary session

or call me at +1 (828) 884-8840.