Why Low Interest Rates Signals Slowdowns, Not Growth

10 mins

By

Jon Green

June 17, 2026

I’ve written about interest rates before, but they are in the news again. And, to be honest, the link between interest rates and the economy are not always clear if you don’t live and breathe economics.

I’ve written about interest rates before, but they are in the news again. And, to be honest, the link between interest rates and the economy are not always clear if you don’t live and breathe economics.

There’s a misconception floating around that low interest rates signal growth. It’s partially true—but mostly incorrect. What is concerning is that we see this myth repeated at the highest levels of government:

“There’s no reason to raise interest rates,” President Trump said in a recent NBC interview. “The country becomes great. We built the country by doing great and having rates low. What they do is when they raise interest rates, they try to kill success. I don’t want to kill success. We should actually lower interest rates.”

This statement is confusing because it's an inaccurate view of how interest rates work. And it's worrying if the current Chair of the Federal Reserve acts on this policy view, because there are negative consequences to lowering the interest rate too soon.

To understand the relationship, let’s first focus on why and how the Federal Reserve uses interest rates.

What are interest rates used for?

Interest rates like your mortgage or auto loan are based on the Federal Fund Rate. Typically, I’ll use these two terms interchangeably. But what you need to remember first, terminology wise: Is that the Federal Fund Rate is the baseline rate that banks use to trade money with each other.

Why do banks trade? Well, if one bank has excess cash and another needs cash to remain stable or meet federal requirements, the first bank lends that extra money to the second.

However, this rate matters more to you and I than one might realize. In COVID, we got a taste of the power of the Federal Fund Rate as the Federal Reserve raised rates to stifle inflation.

In other words, this interest rate directly affects the economy. For analysts and advisors, the Federal Reserve’s decisions to increase or decrease that rate gives us a heads up on federal perspectives of the economy.

Why do interest rates rise with growth?

Interest rates often rise during periods of economic growth, since inflation often follows quality of life improvements. A higher interest rate staggers inflation, a tool that ideally prevents prices from raging out of control.

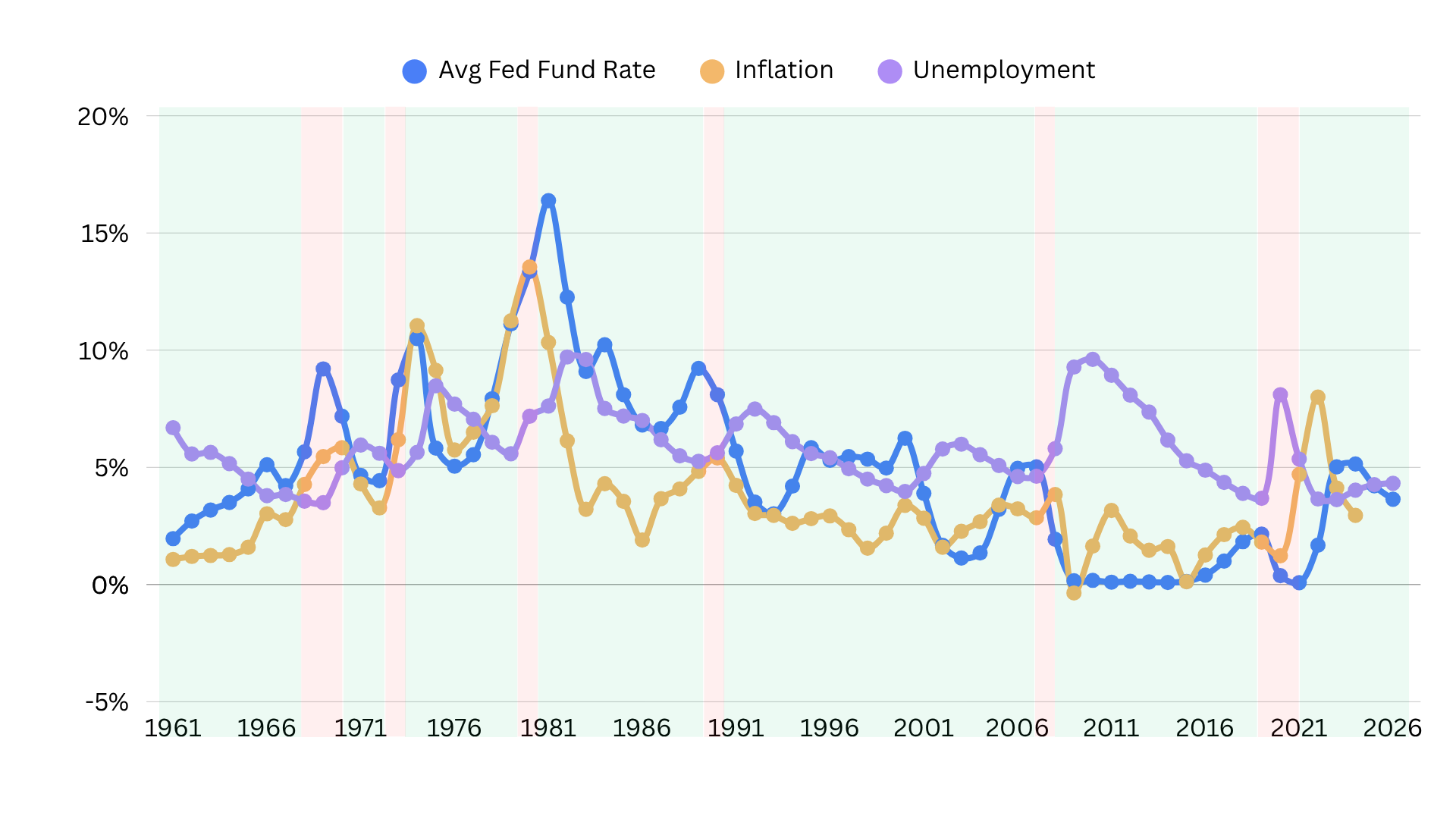

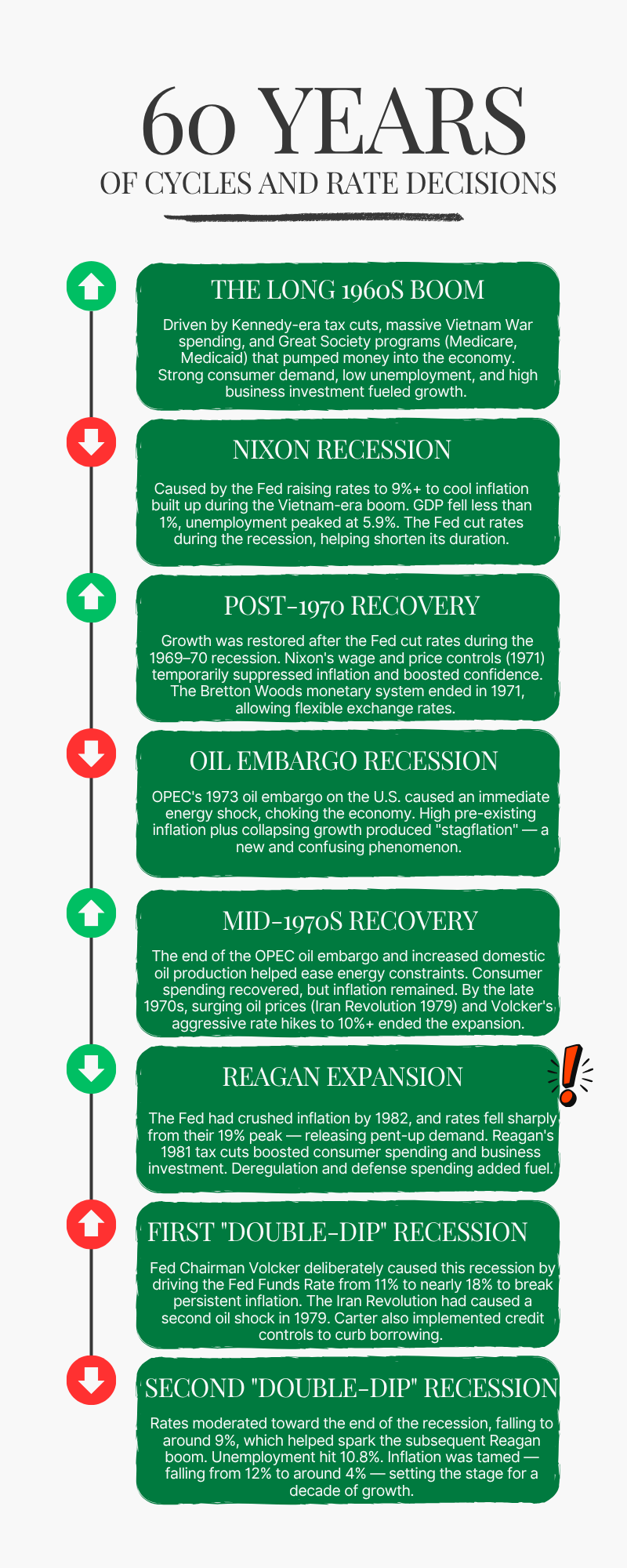

Take the 1960s boom, for example. Interest rates rose from 1.5% to 9% in 10 years to contain inflation stemming from high growth.

Of course, there are exceptions. The only expansion period when interest rates were reduced was during the Reagan Era – dropping from a 19% peak to an average of 8.1% in 1990.

Likewise, interest rates tend to drop when growth slows. Lowering interest rates can incentivize short bursts of consumer spending, whether that be through cash purchases or easier access to capital. Here, interest rates are used not to stop an overheating economy but warm up a cold economic season.

If this was the reasoning behind lowering interest rates today, that might even make sense. Take our current GDP of 1.6%, which seems healthy enough. However, the Economic Policy Institute suggests nearly half of that is solely due to AI—-which itself appears to be a bubble. And when that bubble pops, so does the associated growth.

To get a better understanding of how

America up-close: What the past 60 years say about rates and growth

The following infographics can be used to visualize the connection between economic periods and rates. For the most part, rates rose with inflationary pressures and GDP growth. The only exceptions are really the Reagan Era, the Housing Boom, and COVID.

However, it’s incredibly important to note that these three exceptions offered extenuating circumstances.

First, the Reagan Era lowered rates after record highs. The previous administration had hiked the interest rates in an attempt to combat inflation and surging oil prices following the Iranian Revolution.

The second, the Housing Boom, did encourage spending and GDP growth through lower rates—but when combined with deregulation, it also set the stage for The Great Recession. During this period, GDP fell 4.3% and unemployment soared to 10%.

Finally, COVID was the third exception, a global pandemic does warrant a different approach to economics. Between the near-zero rate cuts and the $2+ trillion in relief packages, the economy rebounded within two months. Technically, anyway.

Of course, most of the time, interest rates rise with growth and sink with downturns. So, why is there a disconnect in the White House on this fundamental principle? And what happens if they decide to drop rates?

Decoding The Disconnect (and What it Means For You)

The simplest answer I can come up with is that the President believes that his era will mirror Reagan’s. However, the current administration is handling a vastly different economy. And as a financial advisor that focuses on risk management, it’s often better to bet on the norm rather than the exception.

Here are a few key differences:

Reagan’s federal tax rate was 70%, the current rate is 37%

Union membership was around 35% while current membership is 10%

Pre-Reagan, the government actively managed demand, invested in infrastructure, and expanded social programs. Since Reagan, many administrations have focused on reducing the government's role, slowing government spending growth, cutting taxes, and deregulating industry.

The National Debt has continued to rise since the Reagan Era

The pre-Reagan economy was heavily industrial and manufacturing-based. The current economy is driven by technology and services.

Just from this data, we can determine that Reagan and Trump have an entirely different set of tools and issues when it comes to the economy. Thus, it’s unlikely that an interest rate cut would result in significant long-term benefits.

There are other concerns. It’s well-known at this point that the current administration leans heavily into the Heritage Foundation’s Project 2025 recommendations. This think-tank goes further than the President. In fact, in its plan, the Heritage Foundation recommends the following from former White House director of the domestic policy council Paul Winfree:

“…Winfree suggests that the next Administration should think about proposing legislation that would “effectively abolish” the Federal Reserve and replace it with “free banking,” whereby “neither interest rates nor the supply of money” would be “controlled by government.””

While that seems wildly unlikely, we find another rationale towards low interest rates in the same document:

“To reduce interest payments on the debt, the Treasury should lock in current relatively low interest rates by issuing longer duration bonds, and even consider creating a 50-year treasury bill.”

At first glance, this appears logical. Reducing interest on the ballooning debt can improve government cash flow. But the National Debt isn’t the only economic issue.

What happens if the Fed lowers interest rates now?

Lower interest rates will initially cause an uptick of spending—ideally, that’s the main benefit. However, when compounded with ongoing inflation and price-gouging, housing affordability, mass deportations resulting in loss of labor, tariffs, and loss of favorable trade agreements, the long-term effect may be increasing inflation.

In addition, lower rates result in lower returns for U.S. Treasury Bonds. It will increase the value of existing bonds, making them more favorable and more sellable in the secondary market. Sold bonds would drain the Treasury of much-needed funds to pay the debt. At the same time, newer bonds would attract fewer buyers. This means less cash flow in the Federal Reserve.

All of this creates instability for consumers in the long-term. Higher prices from inflation combined with less funds for the government pushes our currency value down and stresses the financial system.

The further we strain the system, the more we risk collapse. That affects not only our portfolios and current cash reserves, but our ability to bank safely and make near-future financial decisions.

Want some feedback on your retirement plan? We can help.

With over 40+ years of experience in the financial sector, and as a licensed fiduciary, founder Jon Green can help you look over your retirement plan and understand whether you are on track.

What are we doing over at Encompass Advisors? When we aren’t speaking with clients, we are watching the markets and running numbers. Get our latest, in-depth insights here.

.png)