You may have even asked it yourself.

The question, and sometimes it’s not a question but a demand, sounds simple:

“Could you get me a higher return with no risk?”

When I get this question, I understand where it’s coming from. No one wants to lose their money in the market. Everyone needs a high return to meet retirement goals. In an ideal world, you’d have reward with absolutely no risk.

But that’s not how the market works. Let me explain.

Why this question doesn’t make sense

Normally my answer isn’t just a few words, it’s a walk-through, a snapshot of my research as an advisor.

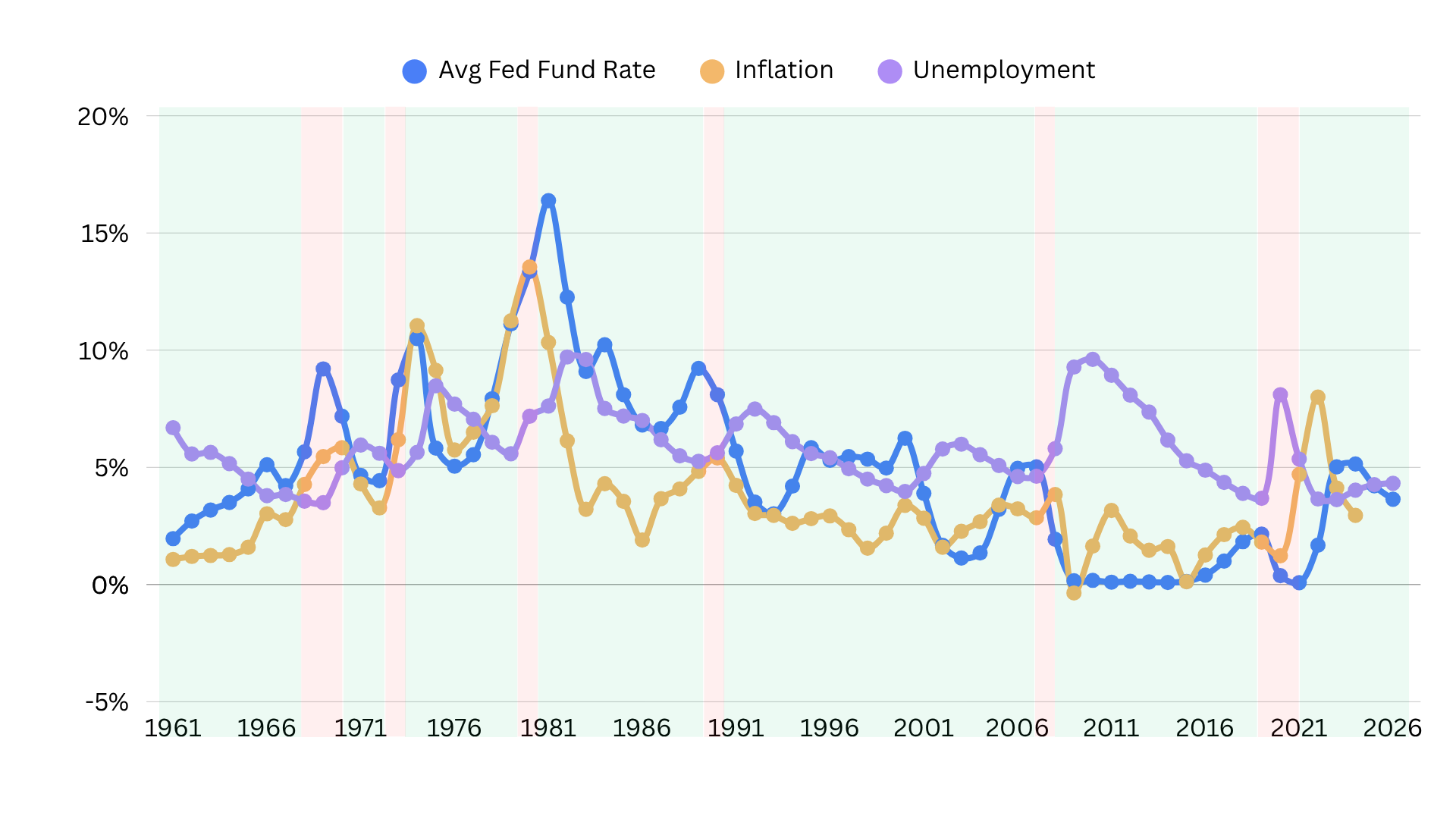

I’ll start with low risk, the historically lowest risk asset on the market: U.S. Treasury Bonds. When I show these to my clients or prospects, these assets are almost immediately turned down. And why shouldn’t they? A 3% interest rate barely covers inflation. That’s not good financial sense.

But the highest-returning assets are often not appealing either. My software tools can determine upsides and downsides—hypothetical gains and losses—for several asset types. For instance, imagine a popular stock with a 40% upside. Everyone would want to invest in that, right? A chance at 40% gains on every dollar is a no-brainier. Until you look at the downside and it’s -128%. Could your portfolio suffer that kind of loss?

This is where your advisor lives (or should live): In a state of constantly weighing risks and rewards, and matching those likelihoods to a level of risk you’re comfortable with.

Balancing risk and return: You can’t have one without the other

Every investment comes with risk. There’s no way to avoid it. Without risks, it’s impossible to have high returns. It’s that gap in the middle where we make our fortunes or lose them.

Yet, there are ways to balance risk.

The first is to know what your level of risk is. How much can you afford to lose, both financially and emotionally? If you know the answers to these two questions, making decisions about risk is a whole lot easier.

It’s also important to note there are different types of risks. When you are working with an advisor, this may not matter as much. Fiduciaries calculate risk profiles and often try to keep clients within the lowest-risk range possible.

For example, I often try to keep clients at or above the 96% percentile of risk. When that percentage goes down, their risk goes up. When that rises, risk goes down and their funds are more secure.

If we break that down, there’s a lot of smaller risk considerations:

- Is the currency used for the investment volatile? Investing with the Indian Rupee is obviously less stable than the US Dollar, but even the dollar faces valuation challenges.

- Inflation risk is another top concern. Will gains be wiped out by inflation, will assets face valuation losses because of inflationary pressures?

- Liquidity risk is another primary risk, because if you can’t sell off your assets, you can’t use the funds. Take bonds during the 2022 interest rate hikes, for example. When interest rates rise, bond price value drops. Investors who sold their bonds prematurely, instead of waiting it out, faced losses.

There are other risks, too, such as market risks, political risks, supply chain risks…the list goes on.

All of these micro-risks add up to an investment’s potential downside—how much you can lose. And at the end of the day, you have to weigh if you are comfortable with that potential loss. It’s okay if you aren’t—that’s logical. But balancing that acceptance with rewards will help you find a more sustainable ratio of risk-reward that doesn’t give you sleepless nights.

Common ways to mitigate risks

According to FINRA’s study of investor perspectives on risk, most people understand risk—it’s mitigation they struggle with. When it comes to willingness to take risks, 30% don’t want to risk anything, while the majority are okay with “average risks.”

Experience in investing often gives individuals the ability to better understand their risk tolerance. Hands-on experience also help investors to better understand mitigating risk strategies. In broad terms, these are:

- Varied asset allocation

- Diversification of assets

- Liquidity fund

- Regular re-balancing based on risk tolerance

I believe everyone should be aware of their risk tolerance in relation to their lifestyle and financial goals—whether they have an advisor or not.

That said, if you are looking for an objective fiduciary advisor to help you navigate the complexities of the market, book a call with me today.

Want a second opinion?

Want some feedback

on your retirement plan? We can help.

With over 40+ years of experience in the financial sector, and as a licensed fiduciary, founder Jon Green can help you look over your retirement plan and understand whether you are on track.

You can book a complimentary session

or call me at +1 (828) 884-8840.